42

GESUNDHEITSPROJEKTE IN ENTWICKLUNGS- UND TRANSFORMATIONSLÄNDERN WELTBANK GRUPPE 6.5.2021 AUSSENWIRTSCHAFTSCENTER WASHINGTON

GESUNDHEITSPROJEKTE IN ENTWICKLUNGS- UND TRANSFORMATIONSLÄNDERN

WELTBANK GRUPPE

6.5.2021

AUSSENWIRTSCHAFTSCENTER

WASHINGTON

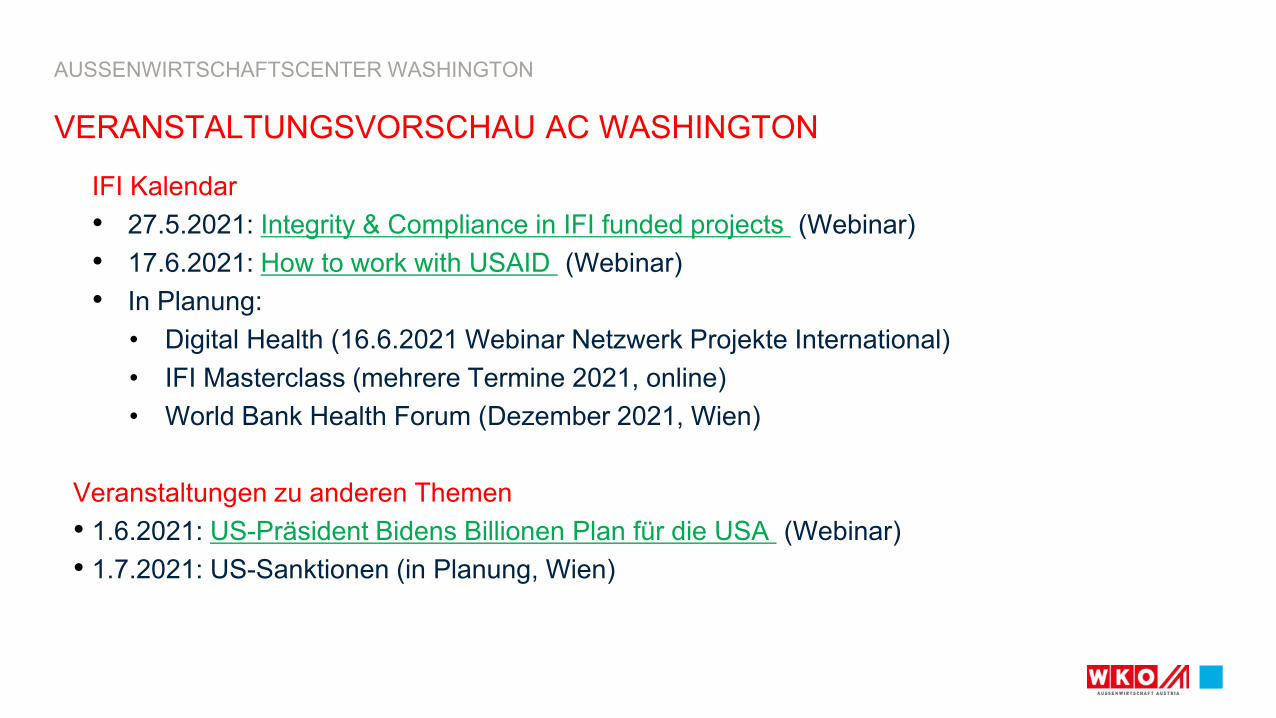

VERANSTALTUNGSVORSCHAU AC WASHINGTON

AUSSENWIRTSCHAFTSCENTER WASHINGTON

IFI Kalendar

• 27.5.2021: Integrity & Compliance in IFI funded projects (Webinar)

• 17.6.2021: How to work with USAID (Webinar)

• In Planung:

• Digital Health (16.6.2021 Webinar Netzwerk Projekte International)

• IFI Masterclass (mehrere Termine 2021, online)

• World Bank Health Forum (Dezember 2021, Wien)

Veranstaltungen zu anderen Themen

• 1.6.2021: US-Präsident Bidens Billionen Plan für die USA (Webinar)

• 1.7.2021: US-Sanktionen (in Planung, Wien)

AUSSENWIRTSCHAFTSCENTER WASHINGTON

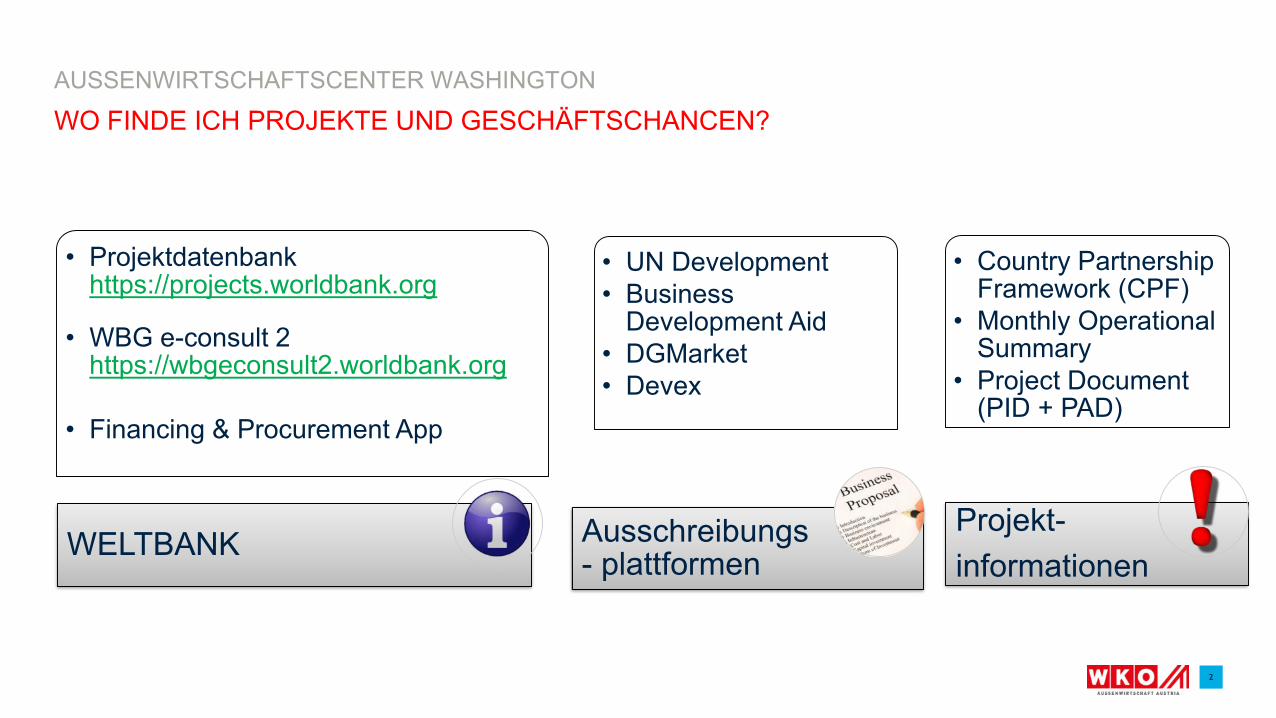

• Projektdatenbankhttps://projects.worldbank.org

• WBG e-consult 2 https://wbgeconsult2.worldbank.org

• Financing & Procurement App

WELTBANK

• UN Development• Business

Development Aid• DGMarket• Devex

Ausschreibungs- plattformen

• Country Partnership Framework (CPF)

• Monthly Operational Summary

• Project Document (PID + PAD)

Projekt-

informationen

WO FINDE ICH PROJEKTE UND GESCHÄFTSCHANCEN?

2

PROJEKTDATENBANK - WELTBANK

AUSSENWIRTSCHAFTSCENTER WASHINGTON

3

AUSSENWIRTSCHAFTSCENTER WASHINGTON

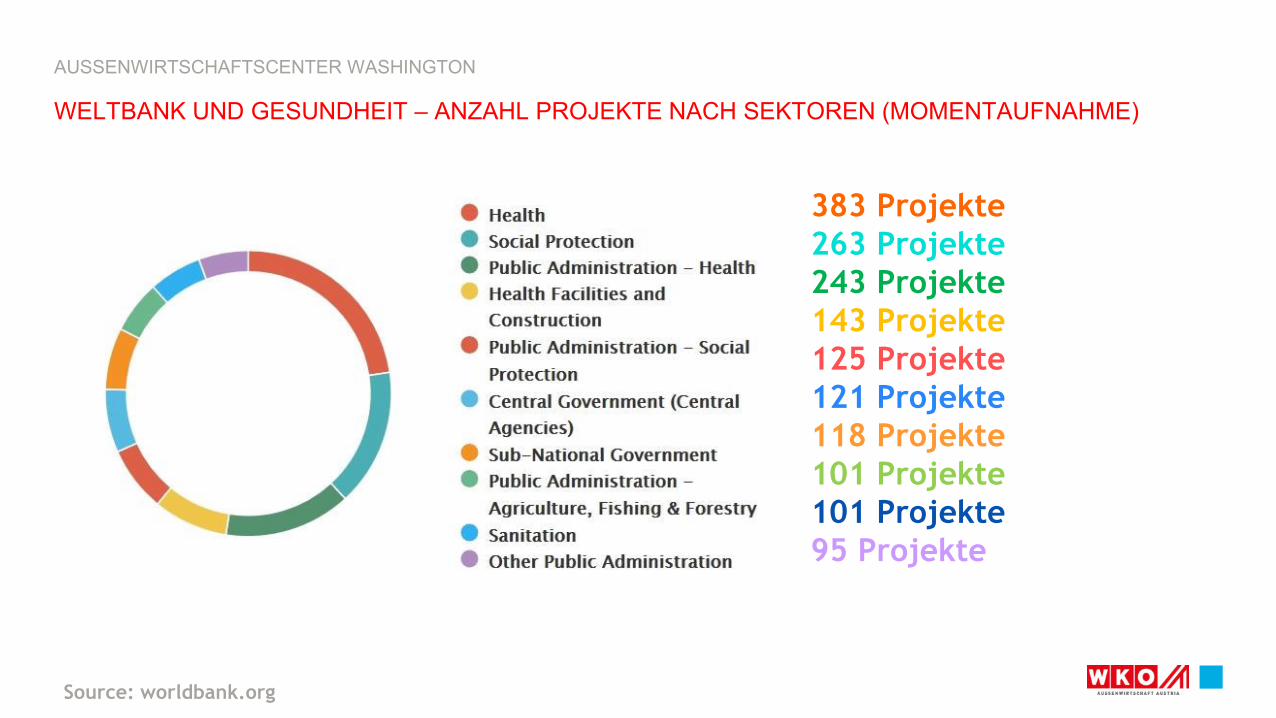

Source: worldbank.org

383 Projekte263 Projekte243 Projekte143 Projekte125 Projekte121 Projekte118 Projekte101 Projekte101 Projekte95 Projekte

WELTBANK UND GESUNDHEIT – ANZAHL PROJEKTE NACH SEKTOREN (MOMENTAUFNAHME)

AUSSENWIRTSCHAFTSCENTER WASHINGTON

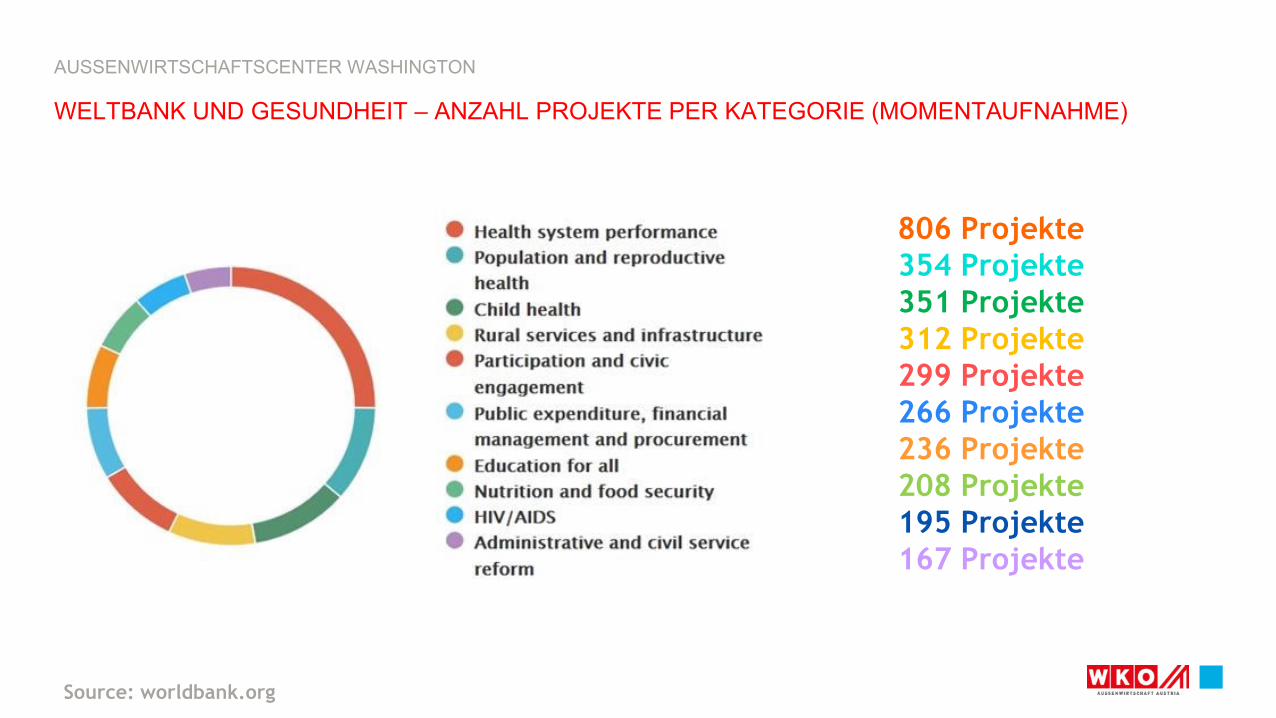

Source: worldbank.org

806 Projekte354 Projekte351 Projekte312 Projekte299 Projekte266 Projekte236 Projekte208 Projekte195 Projekte167 Projekte

WELTBANK UND GESUNDHEIT – ANZAHL PROJEKTE PER KATEGORIE (MOMENTAUFNAHME)

GESUNDHEITSPROJEKTE IN ENTWICKLUNGS- UND TRANSFORMATIONSLÄNDERN

Dr. Andreas Seiter

6. Mai 2021

Outline

• Introduction to the World Bank Group

• Overview of the World Bank’s COVID-19 Response

• The Path Forward: Reimaging Primary Health Care & Creating Effective Delivery Systems

Introduction to the World Bank GroupOur twin goals set a roadmap for sustainable growth and development

End extreme povertyby reducing the share of the global population that lives in extreme poverty (<$1.90 per day)

to 3 percent

Promote shared prosperityby increasing the incomes of the poorest 40

percent of people in every country

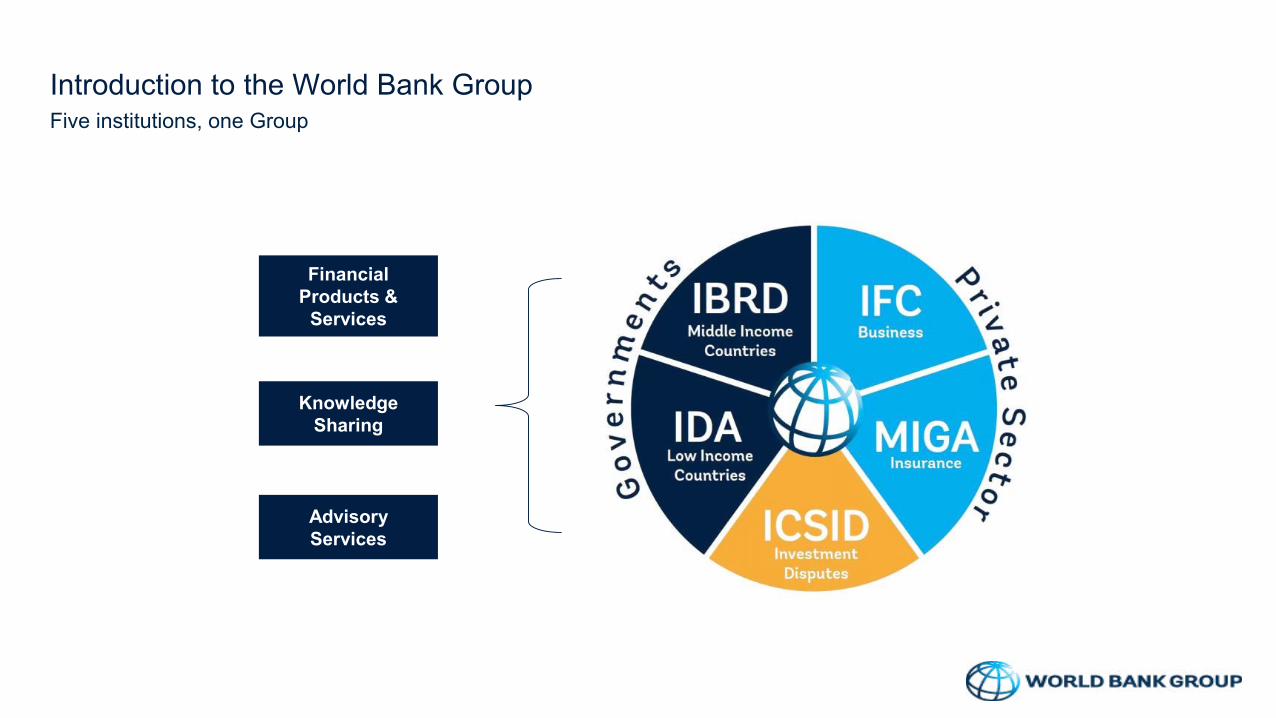

Introduction to the World Bank GroupFive institutions, one Group

Knowledge Sharing

Advisory Services

Financial Products &

Services

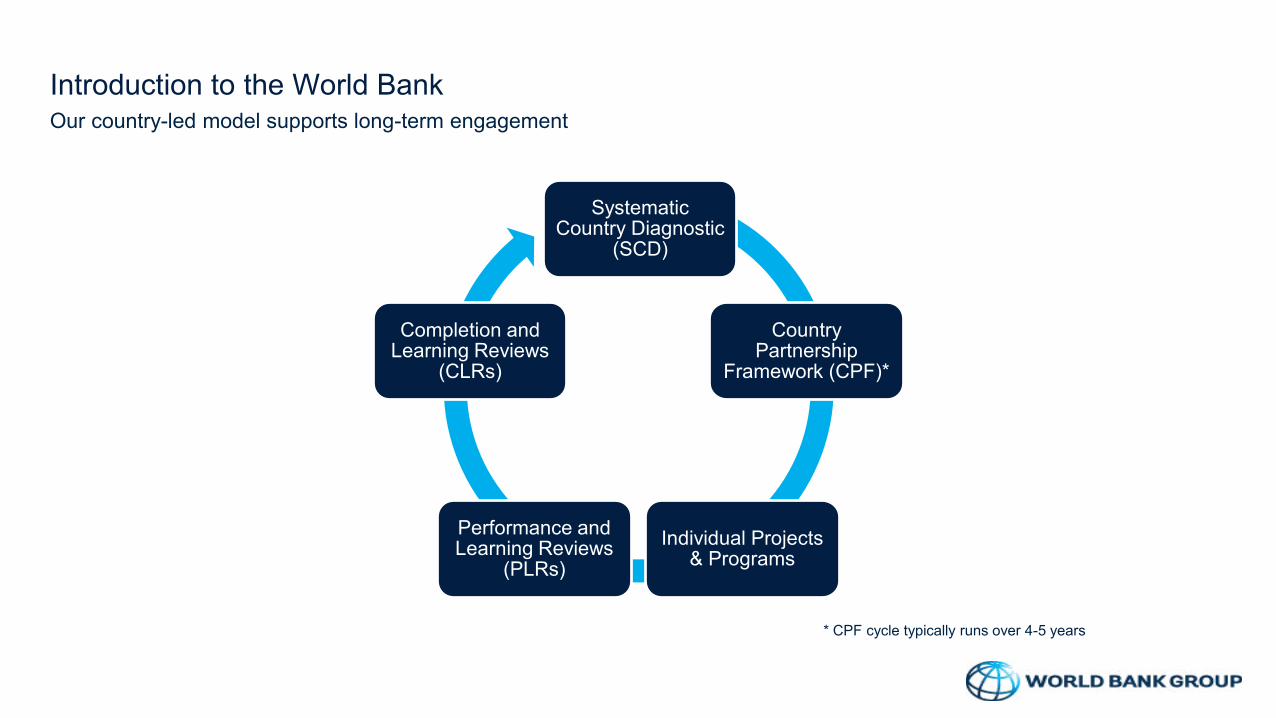

Introduction to the World BankOur country-led model supports long-term engagement

Systematic Country Diagnostic

(SCD)

Country Partnership

Framework (CPF)*

Individual Projects & Programs

Performance and Learning Reviews

(PLRs)

Completion and Learning Reviews

(CLRs)

* CPF cycle typically runs over 4-5 years

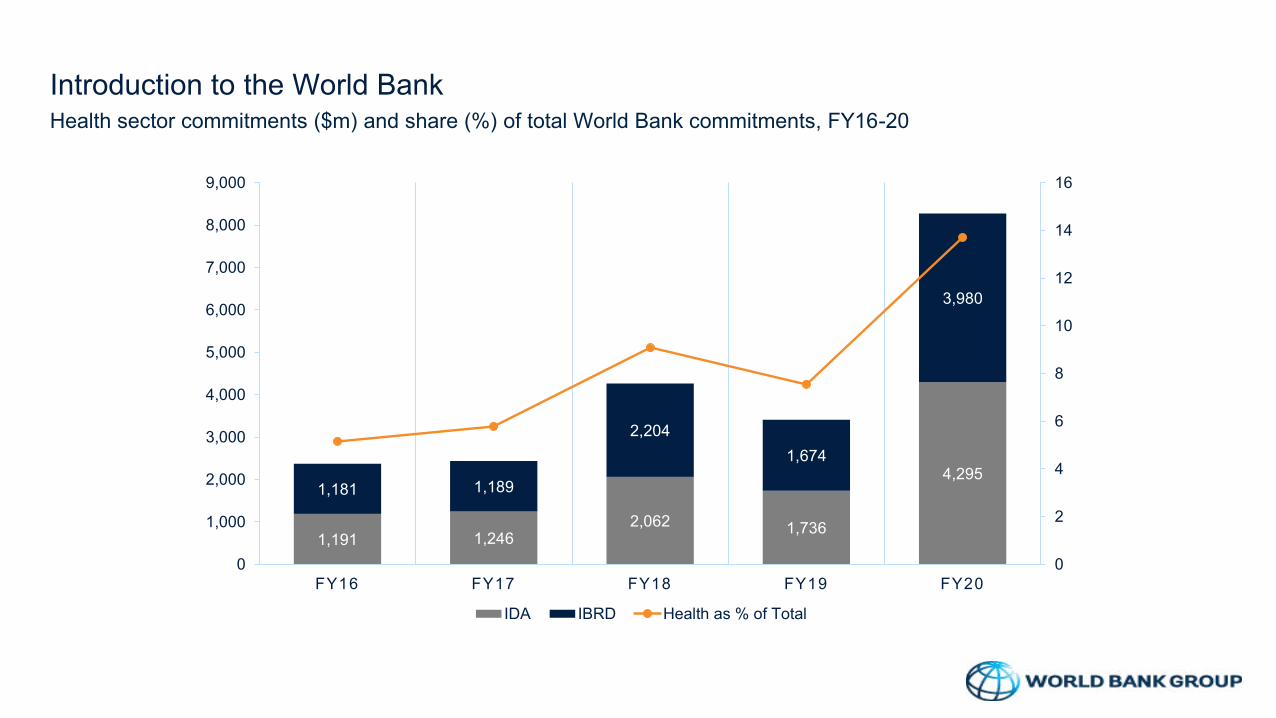

Introduction to the World BankHealth sector commitments ($m) and share (%) of total World Bank commitments, FY16-20

1,191 1,2462,062 1,736

4,2951,181 1,189

2,204

1,674

3,980

0

2

4

6

8

10

12

14

16

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

FY16 FY17 FY18 FY19 FY20

IDA IBRD Health as % of Total

Investment Project Financing (IPF)

• Investment loans, credits and grants provide financing for a wide range of activities, aimed at creating the physical and social infrastructure necessary to reduce poverty and create sustainable development.

• In health, this would typically be investment into infrastructure, training and capacity building, equipment and supplies.

PforR (Program for Results)

1. Finances and supports borrowers’ programs. PforR can support entire programs or subprograms; new

or existing ones; as well as programs that are national or subnational, sectoral or multi-sectoral in nature.

2. Disburses upon achievement of program results.

3. Focuses on strengthening the institutional capacity and the processes and procedures needed for

programs to achieve their desired results

4. Provides assurance that Bank financing is used appropriately, and that the program’s environmental

and social aspects are addressed.

PforR has four main features:

Development Policy Financing (DPF)

• Supports a Member Country's program of policy and institutional actions that promote UHC, for example,

strengthening health financing, improving the quality of care, addressing bottlenecks to improve service

delivery.

• DPF financing helps a borrower address financing requirements through general budget financing that is

subject to the borrower's own implementation processes and systems.

• The Bank makes the funds available to the client upon satisfactory implementation of the overall reform

program; and completion of a set of critical policy and institutional actions agreed between the Bank and the

client.

Strategic priorities for Health, Nutrition and Population (HNP)

1. High Quality Healthcare for All

• Ensure universal and equitable access to affordable, people-centered and integrated quality care with reimagined Primary Healthcare as the foundation of health systems

• Safeguard good governance of health systems for sustainable financing and accountability for health outcomes

• Augment service delivery value chain with innovation, data-driven precision public health and medical care, digital technologies, and private sector accelerators of service delivery

2. Strengthen Public Health

• Reinvigorate essential public health functions for preventive and promotive health, and timely, effective and resilient pandemic preparedness and response

3. Invest in Health beyond Healthcare

• Harness whole-of-Government and multisectoral and institutional response to strengthen Health, Nutrition and Population outcomes

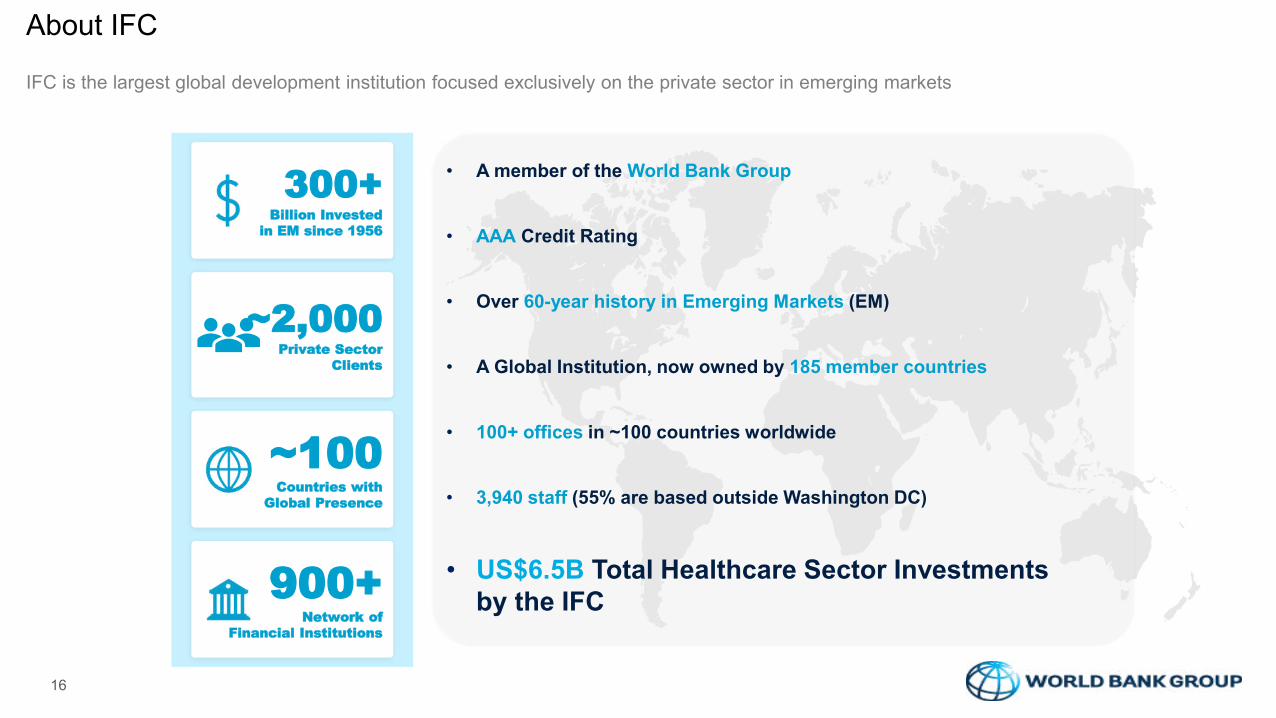

About IFC

16

IFC is the largest global development institution focused exclusively on the private sector in emerging markets

• A member of the World Bank Group

• AAA Credit Rating

• Over 60-year history in Emerging Markets (EM)

• A Global Institution, now owned by 185 member countries

• 100+ offices in ~100 countries worldwide

• 3,940 staff (55% are based outside Washington DC)

• US$6.5B Total Healthcare Sector Investments by the IFC

300+Billion Invested

in EM since 1956

~2,000Private Sector

Clients

~100Countries with

Global Presence

900+Network of

Financial Institutions

Common Trends

D

em

an

d f

or

Healt

hc

are

Changing Population Profile

Increasing Ability to Access Healthcare Services

COVID-19 Impact

Changing Disease Profile

S

up

ply

of

Healt

hc

are

Growing Role for the Private Sector

Evolving Business Models

Digital Health and MedTech Innovations

Health Worker Shortage

Reg

ula

tio

ns

New Regulatory Developments

Global Health Trends

17

Demographics, changes in disease profiles and technology are shifting the healthcare landscape

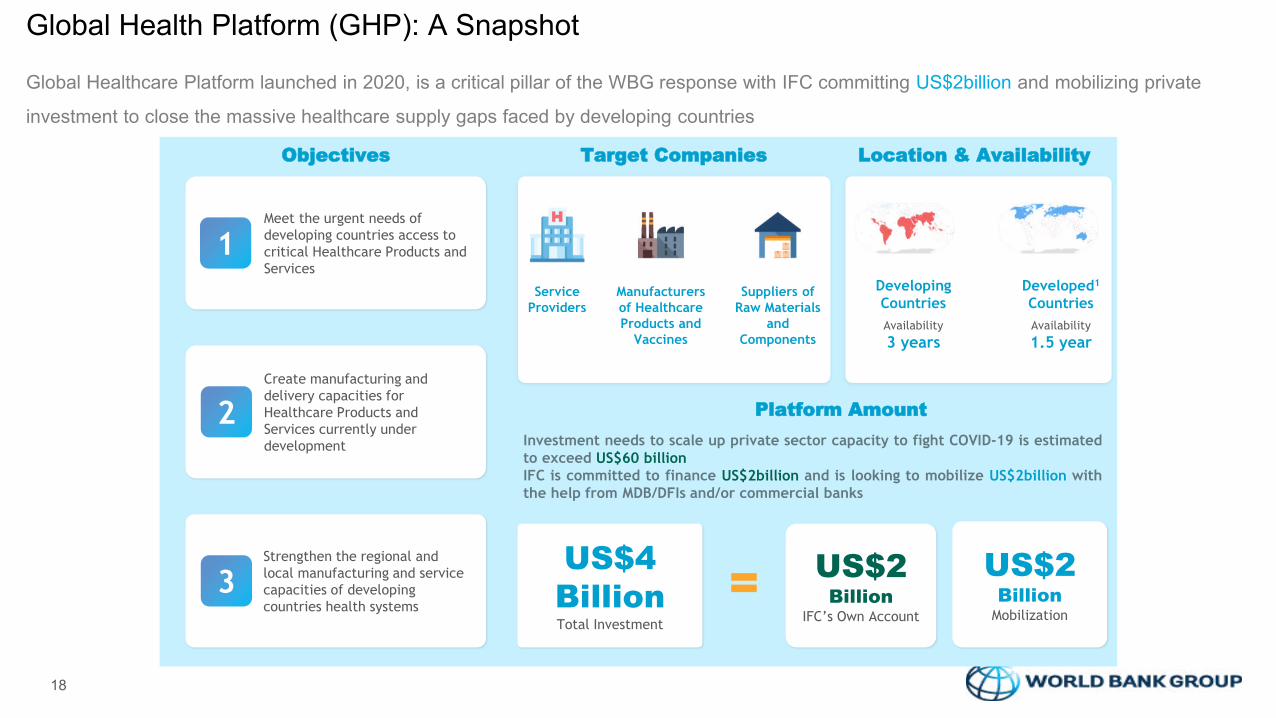

Global Health Platform (GHP): A Snapshot

18

Global Healthcare Platform launched in 2020, is a critical pillar of the WBG response with IFC committing US$2billion and mobilizing private

investment to close the massive healthcare supply gaps faced by developing countries

Meet the urgent needs of developing countries access to critical Healthcare Products and Services

1

Create manufacturing and delivery capacities for Healthcare Products and Services currently under development

2

Strengthen the regional and local manufacturing and service capacities of developing countries health systems

3

Objectives Target Companies

Suppliers of Raw Materials

and Components

Manufacturers of HealthcareProducts and

Vaccines

Service Providers

Location & Availability

Developing Countries

Availability

3 years

Developed1

Countries

Availability

1.5 year

Platform Amount

US$4 BillionTotal Investment

US$2Billion

IFC’s Own Account

US$2Billion

Mobilization

US$60 billionUS$2billion US$2billion

=

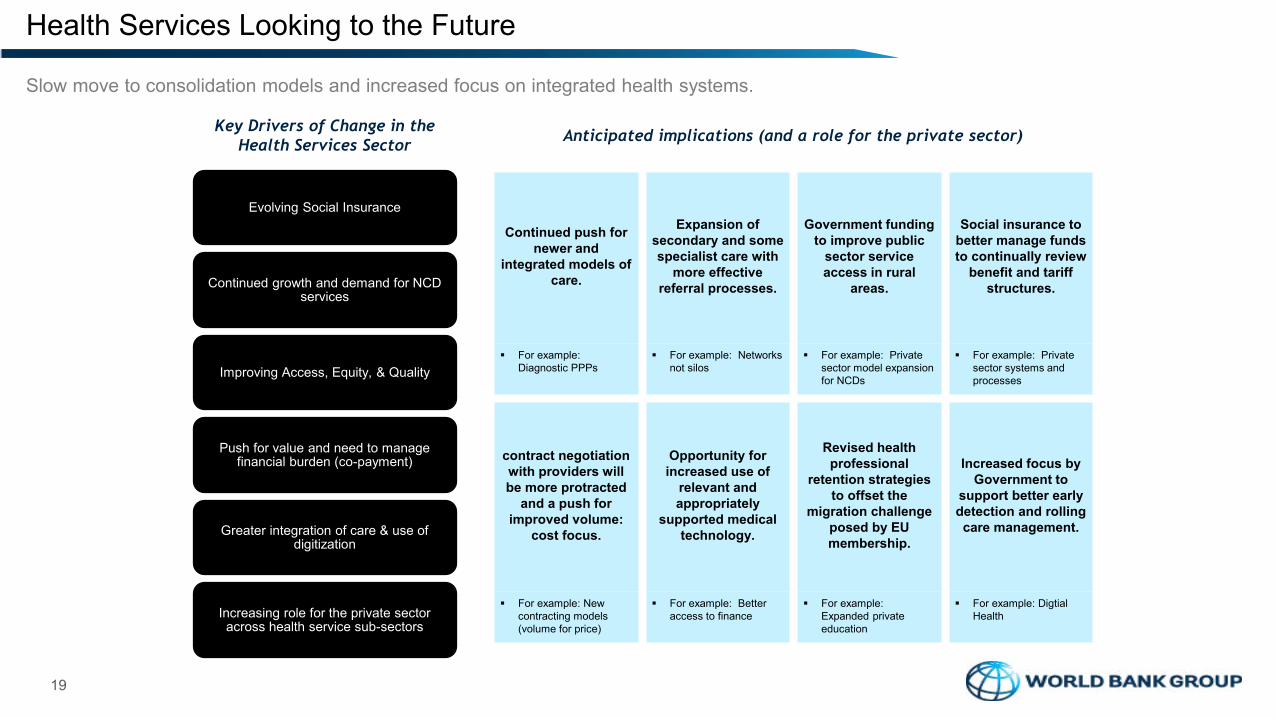

Continued push for newer and

integrated models of care.

Expansion of secondary and some specialist care with

more effective referral processes.

Government fundingto improve public

sector service access in rural

areas.

Social insurance to better manage funds to continually review

benefit and tariff structures.

For example: Diagnostic PPPs

For example: Networks not silos

For example: Private sector model expansion for NCDs

For example: Private sector systems and processes

contract negotiation with providers will be more protracted

and a push for improved volume:

cost focus.

Opportunity forincreased use of

relevant and appropriately

supported medical technology.

Revised health professional

retention strategies to offset the

migration challenge posed by EU membership.

Increased focus by Government to

support better early detection and rolling care management.

For example: New contracting models (volume for price)

For example: Better access to finance

For example: Expanded private education

For example: DigtialHealth

Evolving Social Insurance

Continued growth and demand for NCD services

Improving Access, Equity, & Quality

Push for value and need to manage financial burden (co-payment)

Greater integration of care & use of digitization

Increasing role for the private sector across health service sub-sectors

Slow move to consolidation models and increased focus on integrated health systems.

19

Health Services Looking to the Future

Key Drivers of Change in the Health Services Sector

Anticipated implications (and a role for the private sector)

Ethical Principles in Health Care (EPiHC)

20

Ten fundamental principles, adding clarity to decisions, transactions, practices, and encounters that affect every

aspect of operations

Find more information on the EPiHC initiative and how to become an

EPiHC signatory here: https://www.epihc.org/

Founding Signatories

Respecting Laws and Regulations

Making a Positive Contribution to

Society

Promoting High Quality Standards

Conducting Business Matters Responsibly

Respecting the Environment

Upholding Patients’ Rights

Safeguarding Information & Using

Data Responsibly

Preventing Discrimination,

Harassment, Bullying

Protecting and Empowering Staff

Supporting Ethical Practices and

Preventing Harm

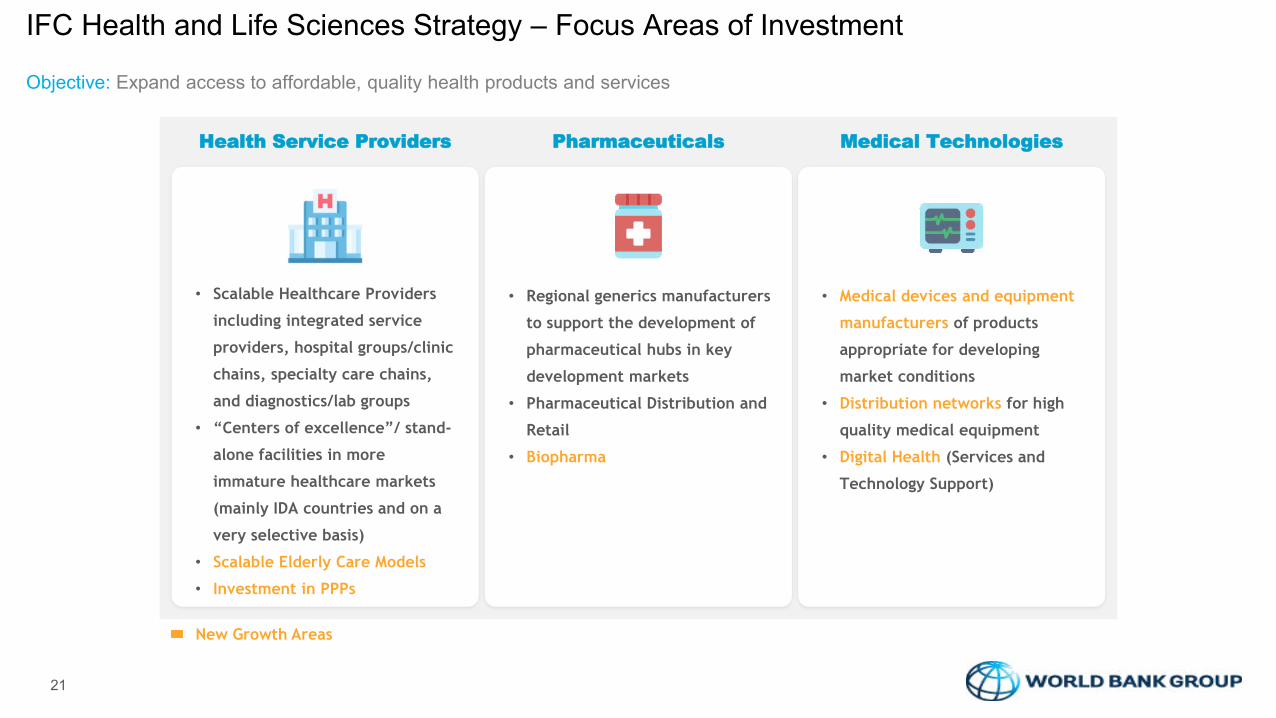

IFC Health and Life Sciences Strategy – Focus Areas of Investment

21

Objective: Expand access to affordable, quality health products and services

Health Service Providers

• Scalable Healthcare Providers

including integrated service

providers, hospital groups/clinic

chains, specialty care chains,

and diagnostics/lab groups

• “Centers of excellence”/ stand-

alone facilities in more

immature healthcare markets

(mainly IDA countries and on a

very selective basis)

• Scalable Elderly Care Models

• Investment in PPPs

• Regional generics manufacturers

to support the development of

pharmaceutical hubs in key

development markets

• Pharmaceutical Distribution and

Retail

• Biopharma

Pharmaceuticals Medical Technologies

• Medical devices and equipment

manufacturers of products

appropriate for developing

market conditions

• Distribution networks for high

quality medical equipment

• Digital Health (Services and

Technology Support)

New Growth Areas

Representative Transactions in Life Sciences & MedTech

22

China

Jointown Pharma$198.5m Debt

2019, 2020

Mexico

Genomma Lab$50.0m Debt

2018

Turkey

Nobel Ilac$25.0m Debt

2017

Mexico

Siegfried$75.0m Debt

$85.0m Mobilization2019

Africa

Trivitron Africa$2.8m Debt

2018

Eastern Africa

Goodlife Pharma$3.0m Debt

2017

Brazil

Farmoquimica$31.0m Debt

$73.0m Mobilization2019

India

Biological E$60.0m Debt

2017

Tanzania

Pyramid Pacific$7.5m Quasi-Equity

2018

Colombia

Procaps$90.0m Equity

2017

China

Weigao$327.7m Debt

2007, 2015, 2020

MENA

Hikma$314.5m Debt and Equity 1987, 1989, 1993, 1994, 2003, 2011, 2012, 2017

India

Glenmark$75.0m Quasi-Equity

2016

China

Essex Bio-Technology$20.0m Quasi-Equity

2016

Africa

Adjuvant (GHIF)$20.0m Fund 1 Equity$25.0m Fund 2 Equity

2013, 20162020

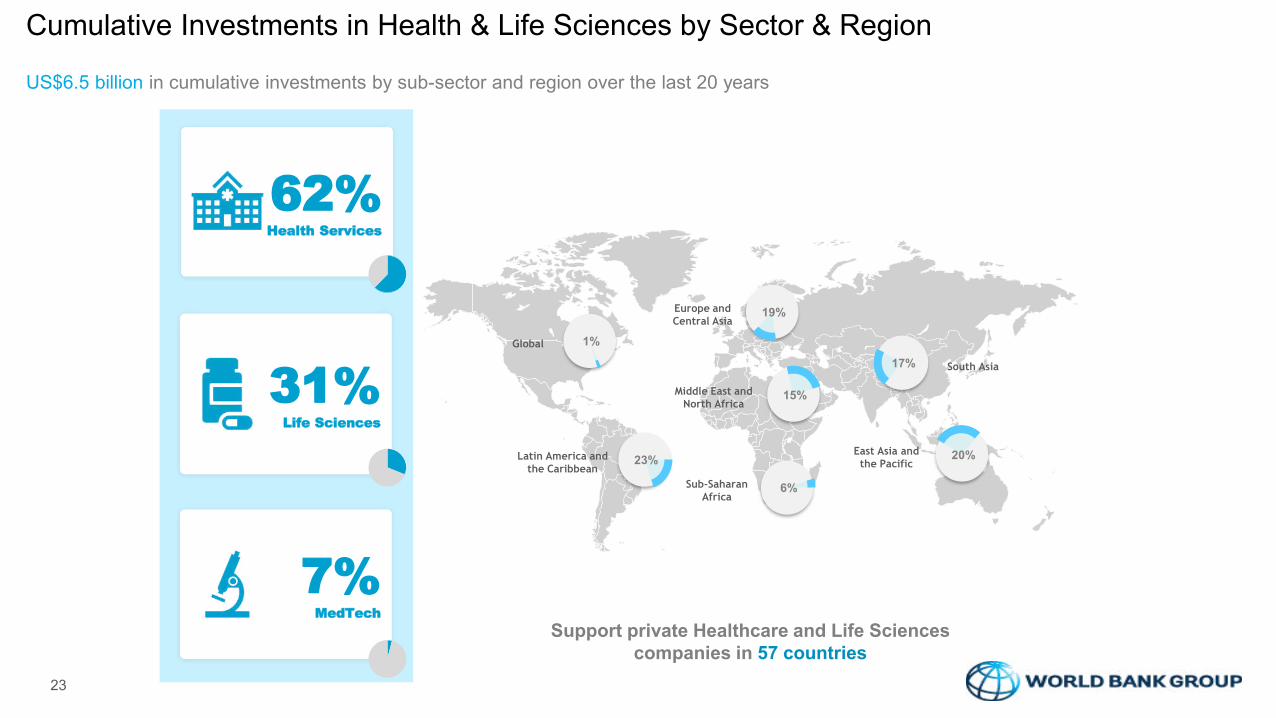

Cumulative Investments in Health & Life Sciences by Sector & Region

23

US$6.5 billion in cumulative investments by sub-sector and region over the last 20 years

Support private Healthcare and Life Sciences companies in 57 countries

23%Latin America and the Caribbean

1%Global

19%Europe and Central Asia

15%Middle East and North Africa

6%Sub-Saharan Africa

17% South Asia

20%East Asia and the Pacific

31%Life Sciences

62%Health Services

7%MedTech

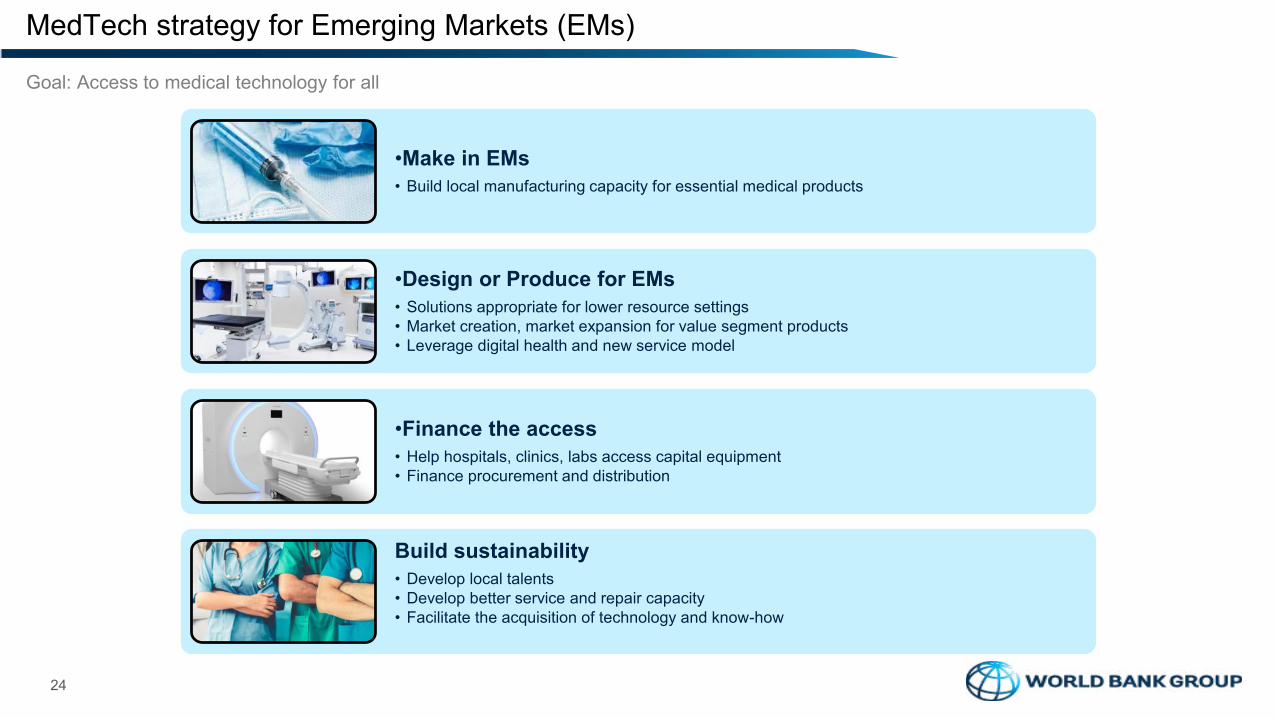

•Make in EMs• Build local manufacturing capacity for essential medical products

•Design or Produce for EMs• Solutions appropriate for lower resource settings• Market creation, market expansion for value segment products• Leverage digital health and new service model

•Finance the access • Help hospitals, clinics, labs access capital equipment• Finance procurement and distribution

Build sustainability• Develop local talents• Develop better service and repair capacity• Facilitate the acquisition of technology and know-how

Goal: Access to medical technology for all

24

MedTech strategy for Emerging Markets (EMs)

25

Up to US$300 m to support healthcare SMEs in 9 African countries

Medical Equipment Financing Facility in Africa

Private healthcare facilities

Manufacturer

IFC

Partner banksAdvisory Services

Risk-Sharing

Loans&

Leases

Products&

Services

Risk-Sharing

Partner Banks50%

IFC40%

OEM10%

Risk Sharing Structurewww.ifc.org/amef

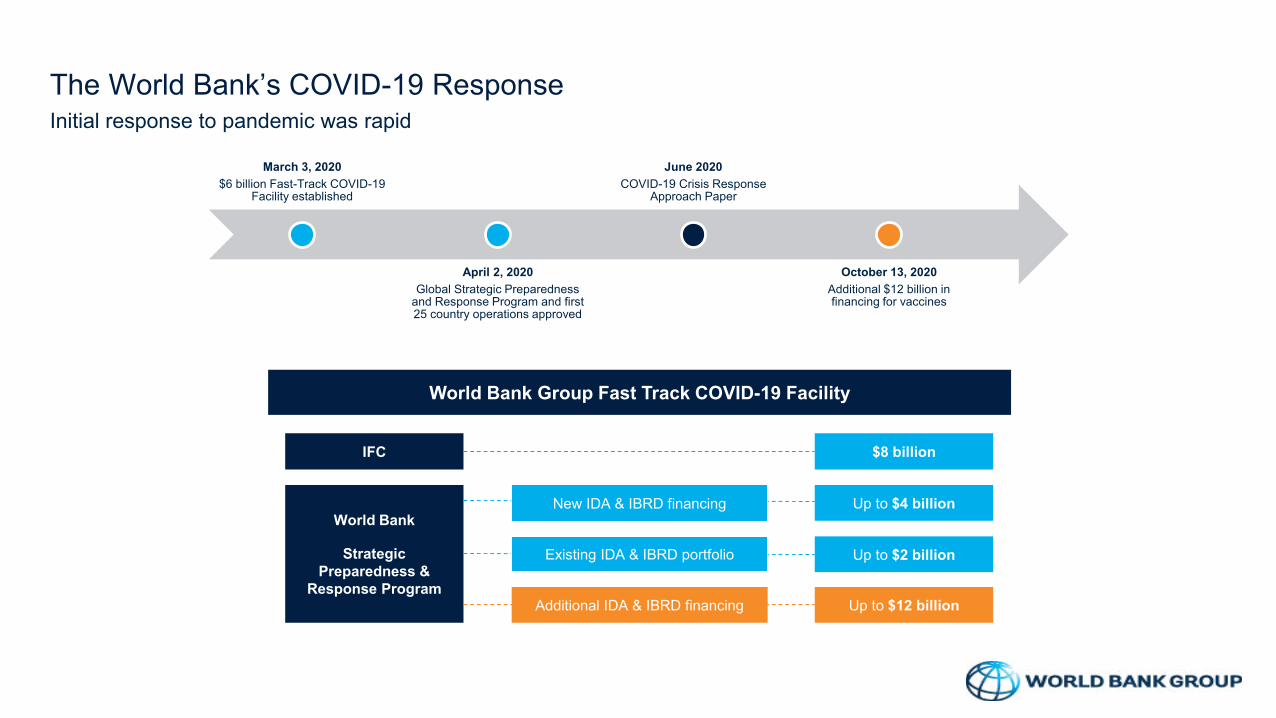

The World Bank’s COVID-19 ResponseInitial response to pandemic was rapid

March 3, 2020

$6 billion Fast-Track COVID-19 Facility established

April 2, 2020

Global Strategic Preparedness and Response Program and first 25 country operations approved

June 2020

COVID-19 Crisis Response Approach Paper

October 13, 2020

Additional $12 billion in financing for vaccines

World Bank Group Fast Track COVID-19 Facility

Up to $4 billion

Up to $2 billion

World Bank

Strategic Preparedness &

Response Program

IFC $8 billion

New IDA & IBRD financing

Existing IDA & IBRD portfolio

Up to $12 billionAdditional IDA & IBRD financing

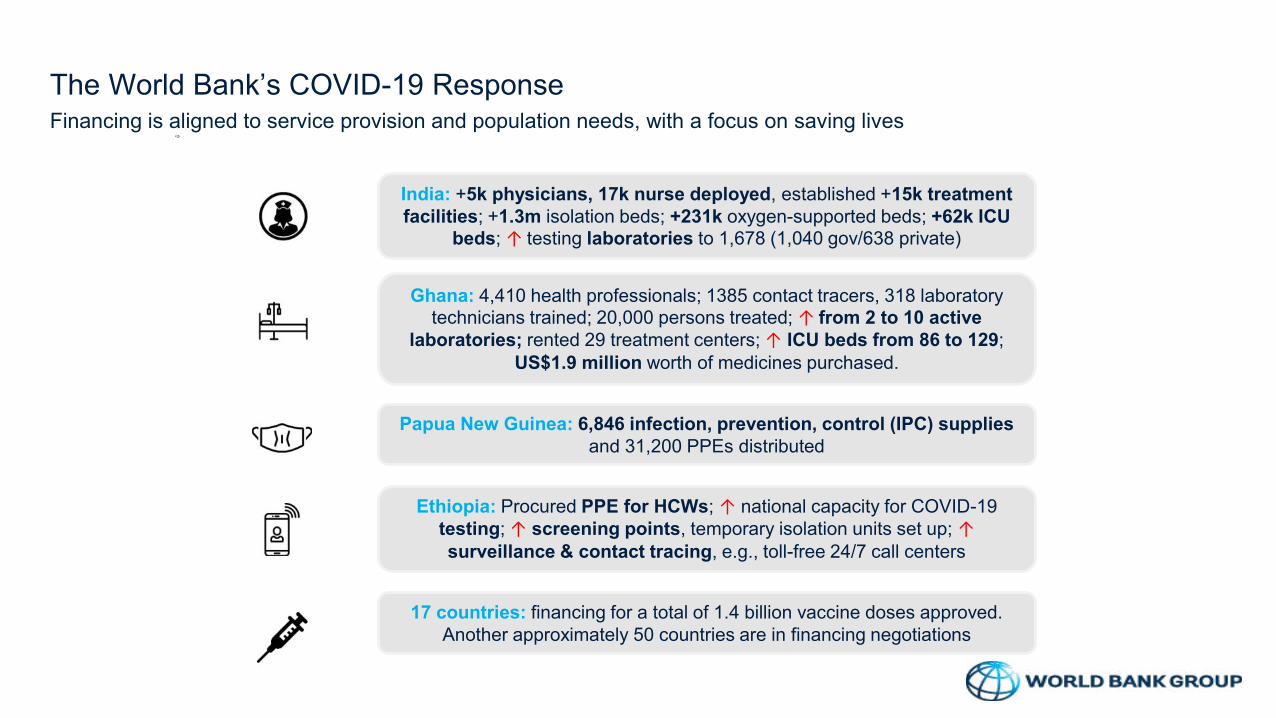

The World Bank’s COVID-19 ResponseFinancing is aligned to service provision and population needs, with a focus on saving lives

Ghana: 4,410 health professionals; 1385 contact tracers, 318 laboratory technicians trained; 20,000 persons treated; ↑ from 2 to 10 active

laboratories; rented 29 treatment centers; ↑ ICU beds from 86 to 129; US$1.9 million worth of medicines purchased.

Papua New Guinea: 6,846 infection, prevention, control (IPC) supplies and 31,200 PPEs distributed

Ethiopia: Procured PPE for HCWs; ↑ national capacity for COVID-19 testing; ↑ screening points, temporary isolation units set up; ↑surveillance & contact tracing, e.g., toll-free 24/7 call centers

India: +5k physicians, 17k nurse deployed, established +15k treatment facilities; +1.3m isolation beds; +231k oxygen-supported beds; +62k ICU

beds; ↑ testing laboratories to 1,678 (1,040 gov/638 private)

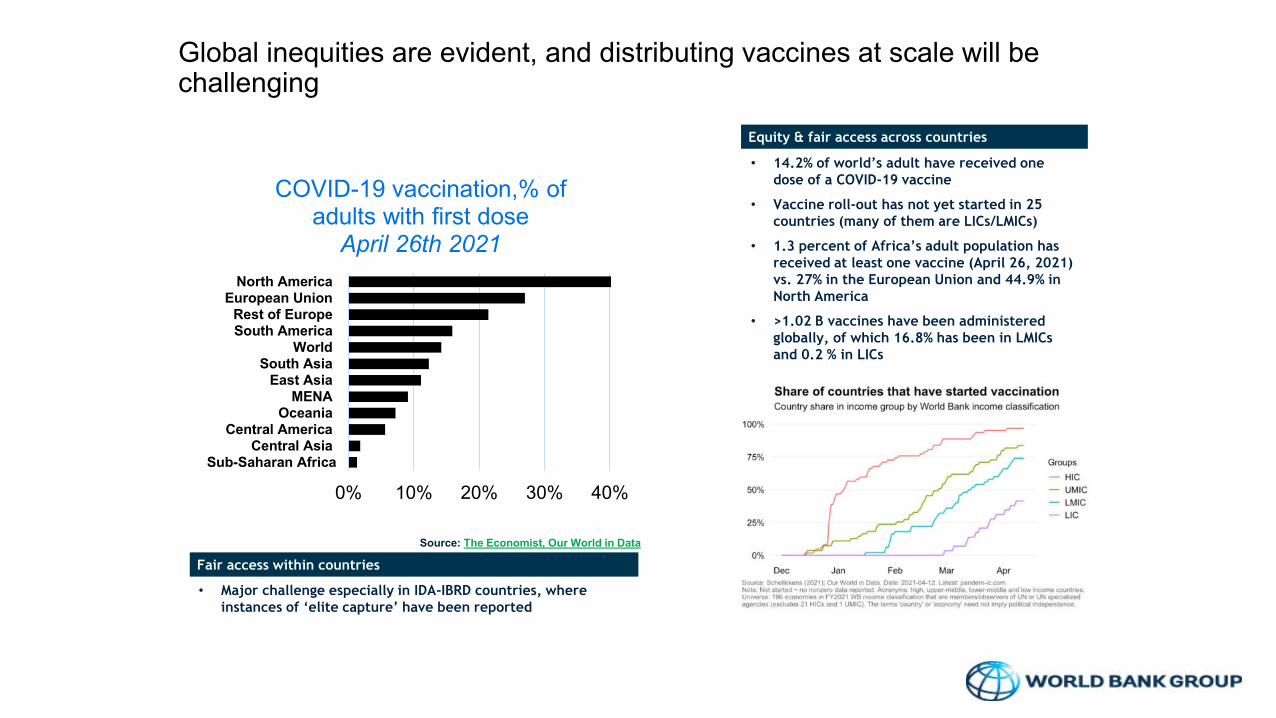

17 countries: financing for a total of 1.4 billion vaccine doses approved. Another approximately 50 countries are in financing negotiations

• 14.2% of world’s adult have received one dose of a COVID-19 vaccine

• Vaccine roll-out has not yet started in 25 countries (many of them are LICs/LMICs)

• 1.3 percent of Africa’s adult population has received at least one vaccine (April 26, 2021) vs. 27% in the European Union and 44.9% in North America

• >1.02 B vaccines have been administered globally, of which 16.8% has been in LMICs and 0.2 % in LICs

• Major challenge especially in IDA-IBRD countries, where instances of ‘elite capture’ have been reported

Global inequities are evident, and distributing vaccines at scale will be challenging

Equity & fair access across countries

Fair access within countries

0% 10% 20% 30% 40%

Sub-Saharan AfricaCentral Asia

Central AmericaOceania

MENAEast Asia

South AsiaWorld

South AmericaRest of Europe

European UnionNorth America

COVID-19 vaccination,% of adults with first dose

April 26th 2021

Source: The Economist, Our World in Data

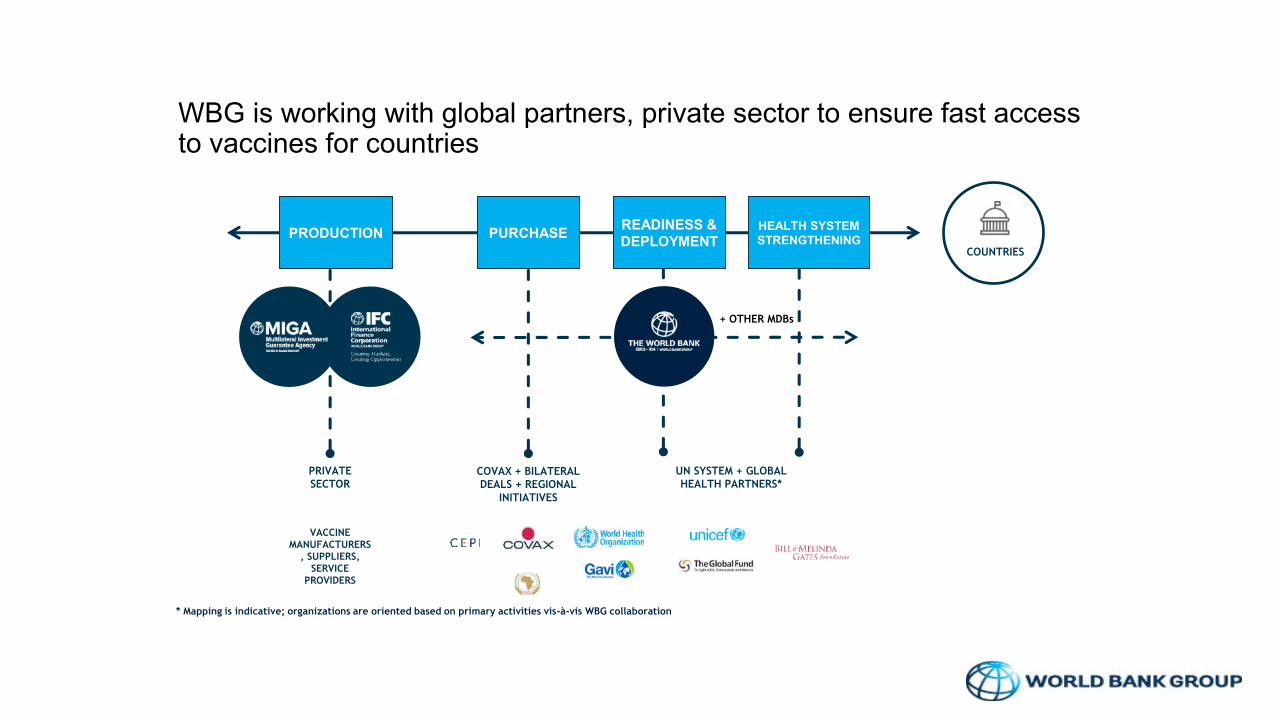

PURCHASE READINESS & DEPLOYMENT

HEALTH SYSTEM STRENGTHENING

WBG is working with global partners, private sector to ensure fast access to vaccines for countries

+ OTHER MDBs

PRIVATE SECTOR

VACCINE MANUFACTURERS

, SUPPLIERS, SERVICE

PROVIDERS

PRODUCTIONCOUNTRIES

* Mapping is indicative; organizations are oriented based on primary activities vis-à-vis WBG collaboration

COVAX + BILATERAL DEALS + REGIONAL

INITIATIVES

UN SYSTEM + GLOBAL HEALTH PARTNERS*

WB’s operational support to countries addresses gaps identified by readiness assessments

PROGRESS IN READINESS

ASSESSMENT ACROSS SELECT

INDICATORS133 countries

reporting

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%100%

PUBLIC CONFIDENCE, TRUST & DEMAND…PROCESSES FOR VACCINE DEPLOYMENT…

COLD CHAIN CAPACITIES ASSESSED

VACCINE SAFETY SYSTEMS IN PLACE

EXPEDITED REGULATORY VACCINE…TARGET POPULATION IDENTIFIED

NATIONAL COORDINATION BODY IN PLACE

NATIONAL DEPLOYMENT VACCINATION…

Yes

In progress

No

Not reported

• 88% of countries have established a national coordinating body for COVID-19 vaccine introduction

• 79% have an expediated regulatory pathway for approval of COVID-19 vaccine in place

• Less than half of the countries have a plan in place to generate public confidence, trust, and demand for COVID-19 vaccines to address demand and hesitancy issues

• Only 52% have process for training vaccinators

STRENGTHS GAPS

• Stakeholder engagement plans are mandatory for all IPF operations and build confidence and trust (e.g., Ethiopia, The Gambia)

• Operations support training of staff involved in deployment and delivery of vaccines (e.g., El Salvador, Ethiopia)

• Most countries putting in place data innovations over the longer-term, to strengthen data and tracking systems and other aspects of health systems (e.g., Cabo Verde)

WB RESPONSE TARGETING GAPS*

*Other includes general COVID health response, systems strengthening, M&E, project

management, training, communication, vaccine storage, regulatory.

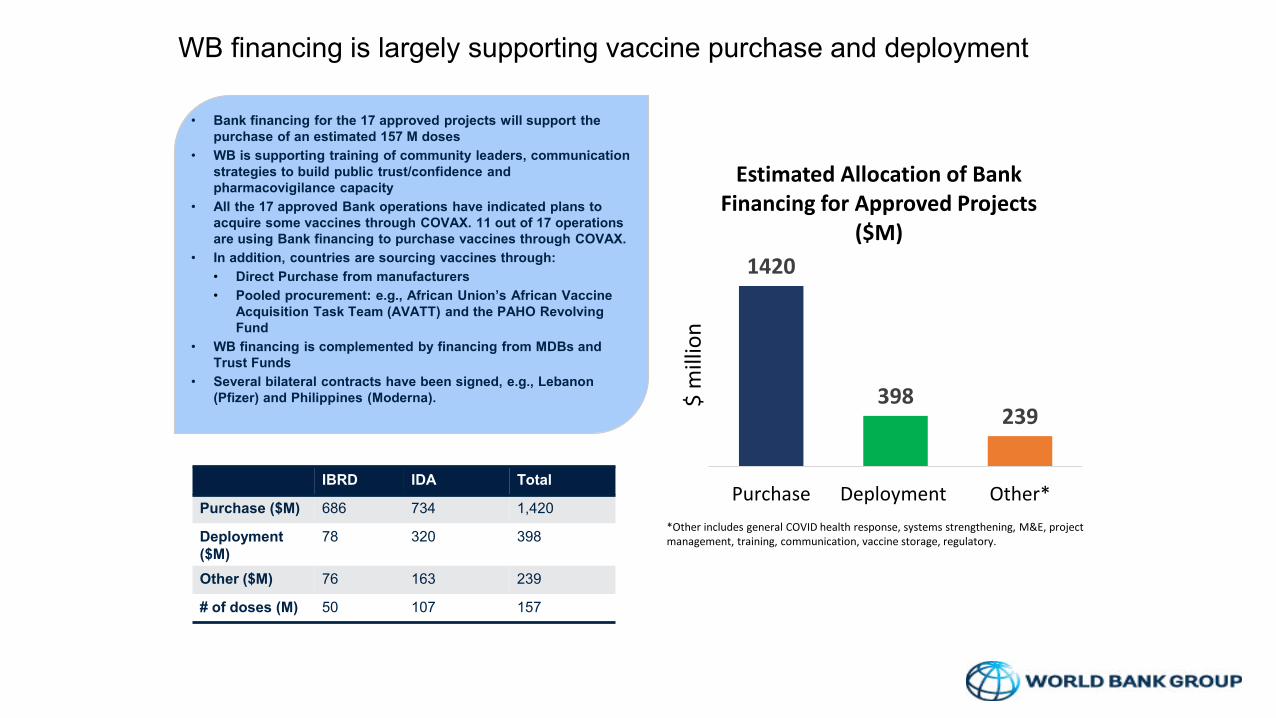

IBRD IDA Total

Purchase ($M) 686 734 1,420

Deployment ($M)

78 320 398

Other ($M) 76 163 239

# of doses (M) 50 107 157

• Bank financing for the 17 approved projects will support the purchase of an estimated 157 M doses

• WB is supporting training of community leaders, communication strategies to build public trust/confidence and pharmacovigilance capacity

• All the 17 approved Bank operations have indicated plans to acquire some vaccines through COVAX. 11 out of 17 operations are using Bank financing to purchase vaccines through COVAX.

• In addition, countries are sourcing vaccines through:

• Direct Purchase from manufacturers

• Pooled procurement: e.g., African Union’s African Vaccine Acquisition Task Team (AVATT) and the PAHO Revolving Fund

• WB financing is complemented by financing from MDBs and Trust Funds

• Several bilateral contracts have been signed, e.g., Lebanon (Pfizer) and Philippines (Moderna).

1420

398239

Purchase Deployment Other*

$ m

illio

n

Estimated Allocation of Bank

Financing for Approved Projects

($M)

WB financing is largely supporting vaccine purchase and deployment

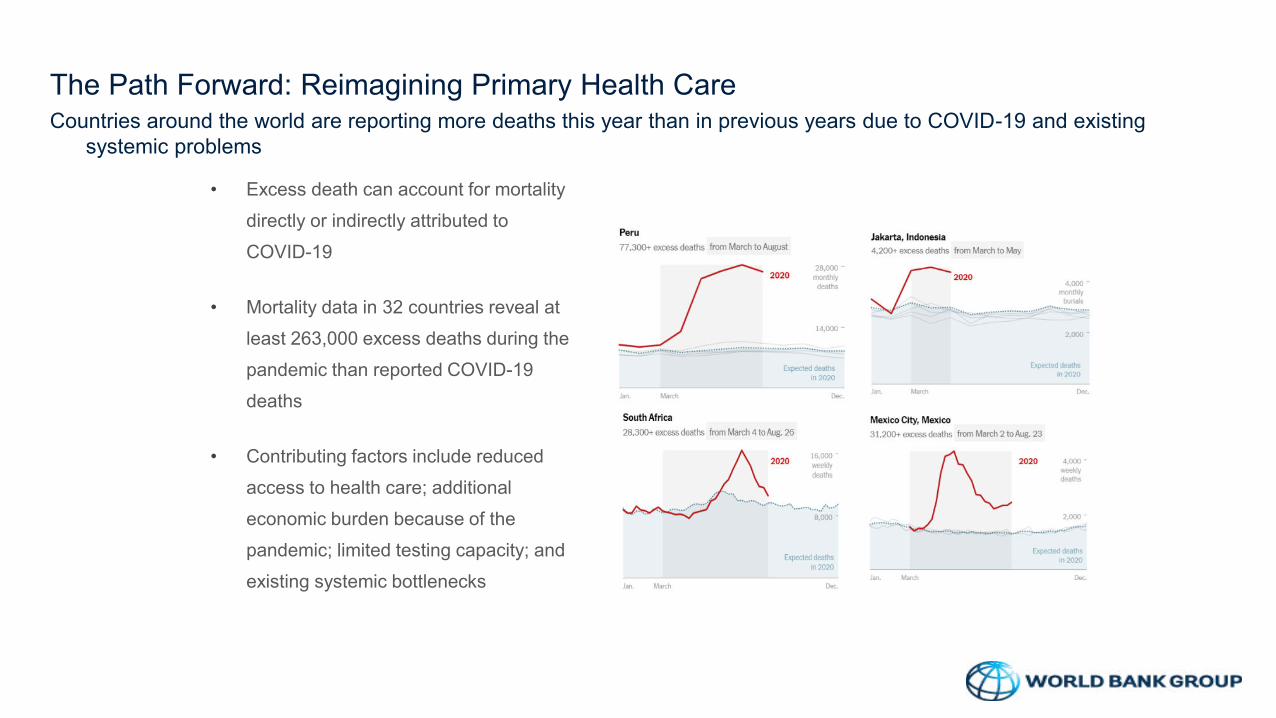

The Path Forward: Reimagining Primary Health CareCountries around the world are reporting more deaths this year than in previous years due to COVID-19 and existing

systemic problems

• Excess death can account for mortality

directly or indirectly attributed to

COVID-19

• Mortality data in 32 countries reveal at

least 263,000 excess deaths during the

pandemic than reported COVID-19

deaths

• Contributing factors include reduced

access to health care; additional

economic burden because of the

pandemic; limited testing capacity; and

existing systemic bottlenecks

The Path Forward: Reimagining Primary Health Care

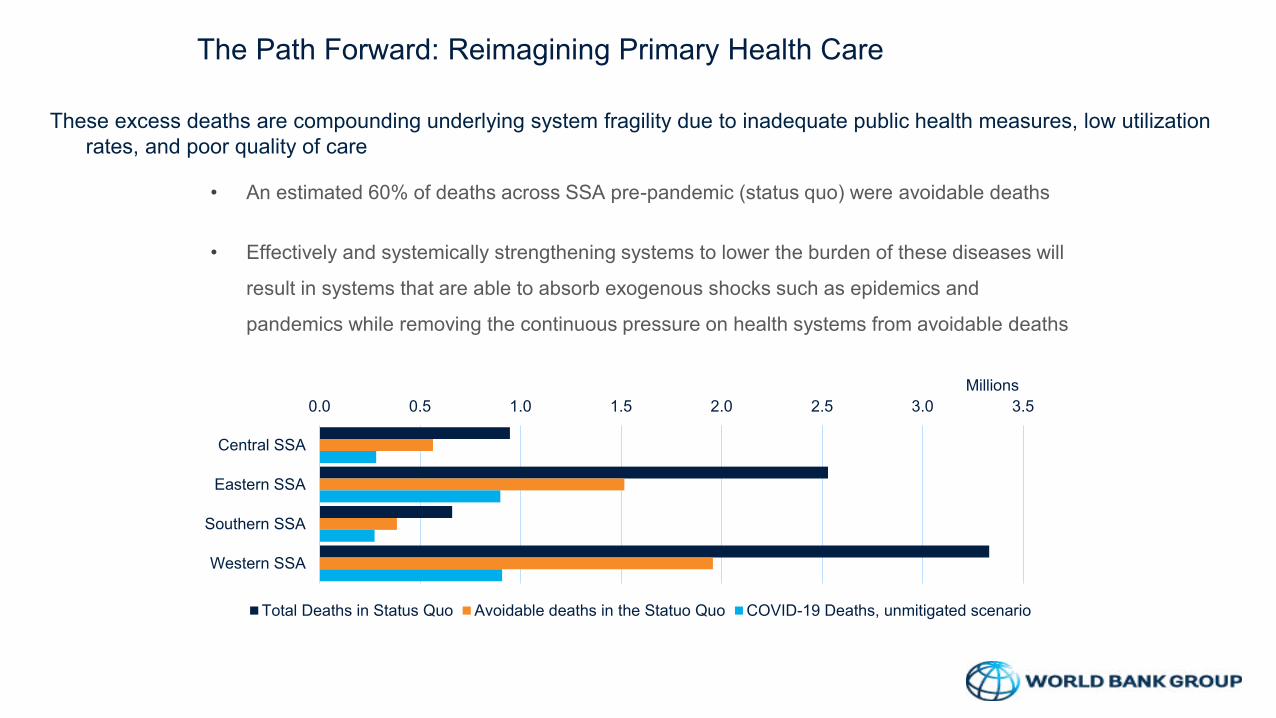

These excess deaths are compounding underlying system fragility due to inadequate public health measures, low utilization rates, and poor quality of care

• An estimated 60% of deaths across SSA pre-pandemic (status quo) were avoidable deaths

• Effectively and systemically strengthening systems to lower the burden of these diseases will

result in systems that are able to absorb exogenous shocks such as epidemics and

pandemics while removing the continuous pressure on health systems from avoidable deaths

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5

Central SSA

Eastern SSA

Southern SSA

Western SSA

Millions

Total Deaths in Status Quo Avoidable deaths in the Statuo Quo COVID-19 Deaths, unmitigated scenario

The Path Forward: Reimagining Primary Health Care

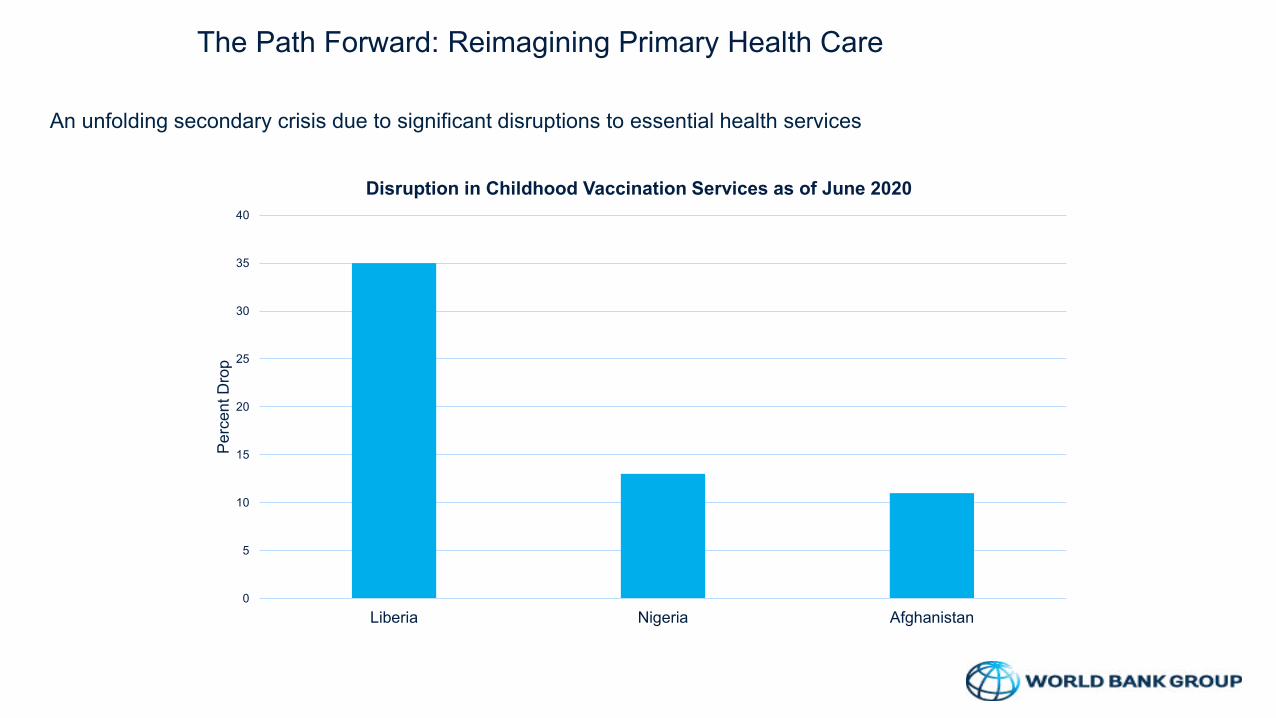

An unfolding secondary crisis due to significant disruptions to essential health services

0

5

10

15

20

25

30

35

40

Liberia Nigeria Afghanistan

Pe

rcen

t D

rop

Disruption in Childhood Vaccination Services as of June 2020

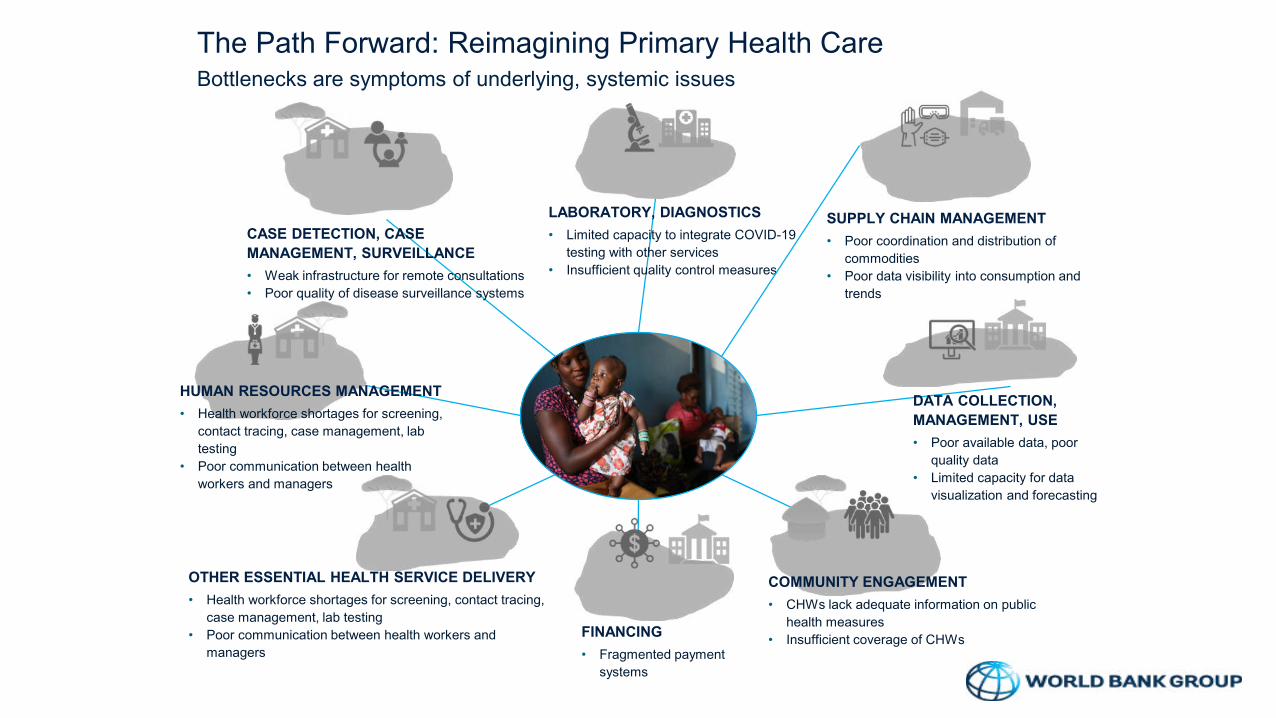

The Path Forward: Reimagining Primary Health CareBottlenecks are symptoms of underlying, systemic issues

SUPPLY CHAIN MANAGEMENT

• Poor coordination and distribution of commodities

• Poor data visibility into consumption and trends

CASE DETECTION, CASE MANAGEMENT, SURVEILLANCE

• Weak infrastructure for remote consultations• Poor quality of disease surveillance systems

LABORATORY, DIAGNOSTICS

• Limited capacity to integrate COVID-19 testing with other services

• Insufficient quality control measures

FINANCING

• Fragmented payment systems

COMMUNITY ENGAGEMENT

• CHWs lack adequate information on public health measures

• Insufficient coverage of CHWs

OTHER ESSENTIAL HEALTH SERVICE DELIVERY

• Health workforce shortages for screening, contact tracing, case management, lab testing

• Poor communication between health workers and managers

HUMAN RESOURCES MANAGEMENT

• Health workforce shortages for screening, contact tracing, case management, lab testing

• Poor communication between health workers and managers

DATA COLLECTION, MANAGEMENT, USE

• Poor available data, poor quality data

• Limited capacity for data visualization and forecasting

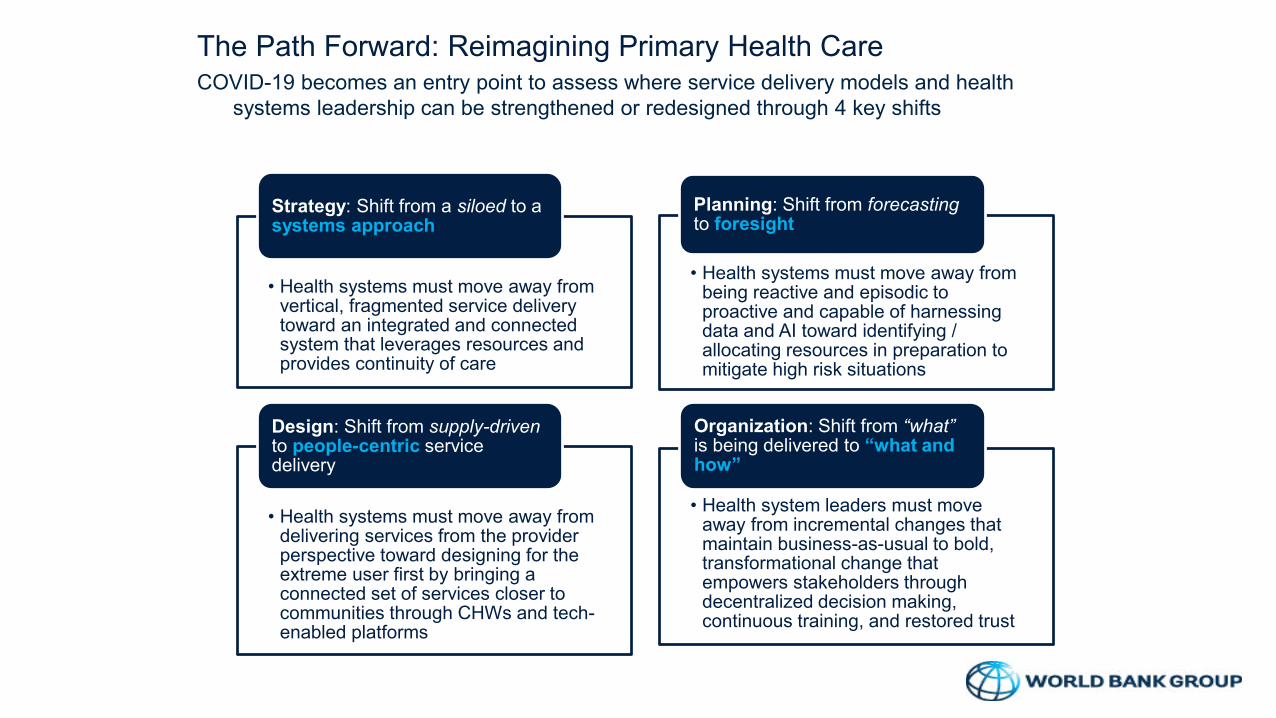

The Path Forward: Reimagining Primary Health CareCOVID-19 becomes an entry point to assess where service delivery models and health

systems leadership can be strengthened or redesigned through 4 key shifts

• Health systems must move away from vertical, fragmented service delivery toward an integrated and connected system that leverages resources and provides continuity of care

Strategy: Shift from a siloed to a systems approach

• Health systems must move away from delivering services from the provider perspective toward designing for the extreme user first by bringing a connected set of services closer to communities through CHWs and tech-enabled platforms

Design: Shift from supply-drivento people-centric service delivery

• Health systems must move away from being reactive and episodic to proactive and capable of harnessing data and AI toward identifying / allocating resources in preparation to mitigate high risk situations

Planning: Shift from forecastingto foresight

• Health system leaders must move away from incremental changes that maintain business-as-usual to bold, transformational change that empowers stakeholders through decentralized decision making, continuous training, and restored trust

Organization: Shift from “what” is being delivered to “what and how”

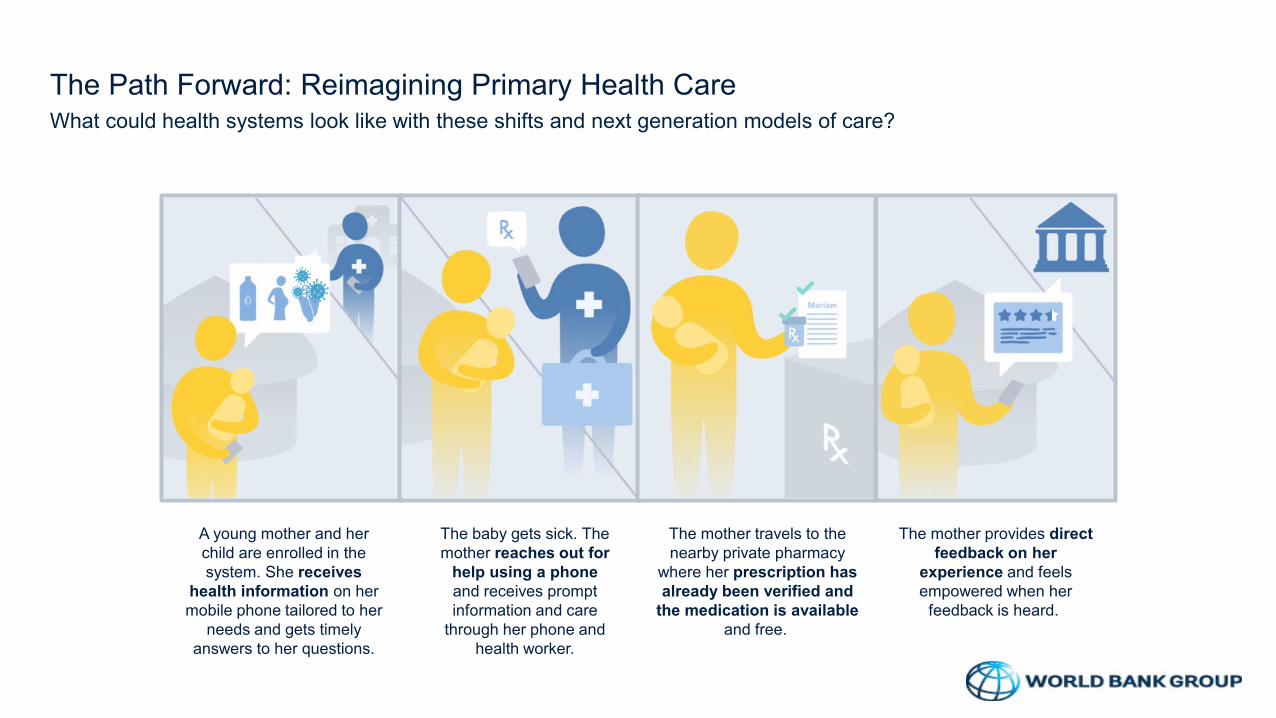

A young mother and her child are enrolled in the system. She receives

health information on her mobile phone tailored to her

needs and gets timely answers to her questions.

The baby gets sick. The mother reaches out for

help using a phone and receives prompt information and care

through her phone and health worker.

The mother travels to the nearby private pharmacy

where her prescription has already been verified and

the medication is available and free.

The mother provides direct feedback on her

experience and feels empowered when her

feedback is heard.

The Path Forward: Reimagining Primary Health CareWhat could health systems look like with these shifts and next generation models of care?

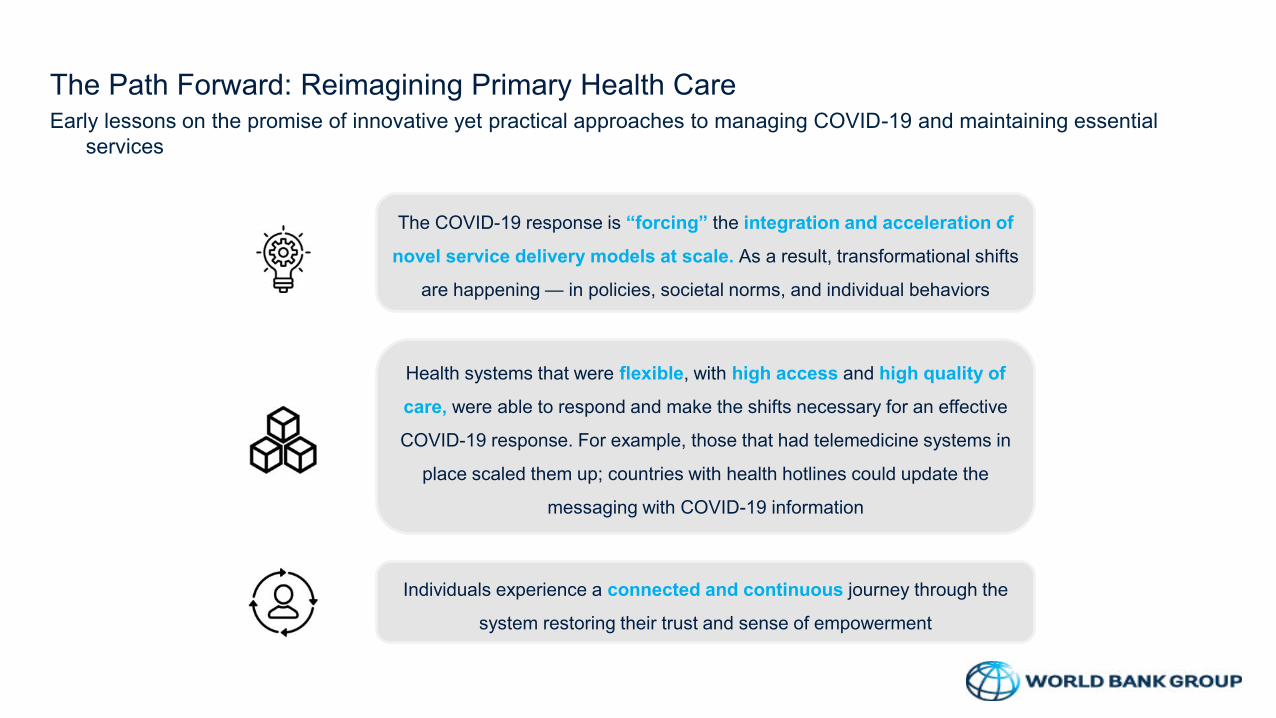

The Path Forward: Reimagining Primary Health CareEarly lessons on the promise of innovative yet practical approaches to managing COVID-19 and maintaining essential

services

The COVID-19 response is “forcing” the integration and acceleration of

novel service delivery models at scale. As a result, transformational shifts

are happening — in policies, societal norms, and individual behaviors

Health systems that were flexible, with high access and high quality of

care, were able to respond and make the shifts necessary for an effective

COVID-19 response. For example, those that had telemedicine systems in

place scaled them up; countries with health hotlines could update the

messaging with COVID-19 information

Individuals experience a connected and continuous journey through the

system restoring their trust and sense of empowerment

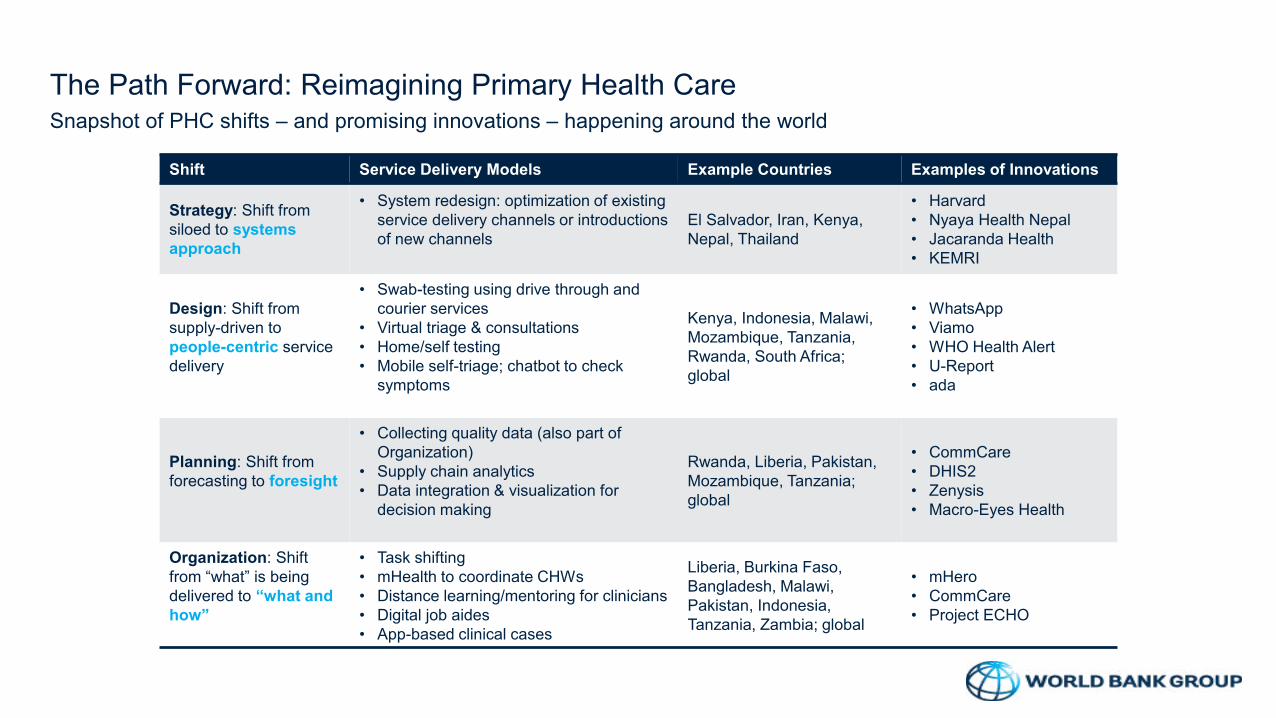

The Path Forward: Reimagining Primary Health CareSnapshot of PHC shifts – and promising innovations – happening around the world

Shift Service Delivery Models Example Countries Examples of Innovations

Strategy: Shift from siloed to systems approach

• System redesign: optimization of existing service delivery channels or introductions of new channels

El Salvador, Iran, Kenya, Nepal, Thailand

• Harvard• Nyaya Health Nepal• Jacaranda Health• KEMRI

Design: Shift from supply-driven to people-centric service delivery

• Swab-testing using drive through and courier services

• Virtual triage & consultations• Home/self testing• Mobile self-triage; chatbot to check

symptoms

Kenya, Indonesia, Malawi, Mozambique, Tanzania, Rwanda, South Africa; global

• WhatsApp• Viamo• WHO Health Alert• U-Report• ada

Planning: Shift from forecasting to foresight

• Collecting quality data (also part of Organization)

• Supply chain analytics• Data integration & visualization for

decision making

Rwanda, Liberia, Pakistan, Mozambique, Tanzania; global

• CommCare• DHIS2• Zenysis• Macro-Eyes Health

Organization: Shift from “what” is being delivered to “what and how”

• Task shifting• mHealth to coordinate CHWs• Distance learning/mentoring for clinicians• Digital job aides• App-based clinical cases

Liberia, Burkina Faso, Bangladesh, Malawi, Pakistan, Indonesia, Tanzania, Zambia; global

• mHero• CommCare• Project ECHO

CDC Jeffrey P. Koplan Lecture 2020

Thank you

Dr. Irene Lack-Hageneder / Mag. Teresa Weiss

AUSSENWIRTSCHAFTSCENTER WASHINGTON

T +1 202 656 0060

ÜBER IHRE FRAGEN FREUEN WIR UNS!

41