LBST.de 23 November 2016 Ludwig-Bölkow-Systemtechnik GmbH VDI-Fachtagung «Innovative Antriebe» ∙ Dresden ∙ 23. November 2016 Erneuerbare Energien im Verkehr 2050 Ergebnisse und Gedankenfutter aus fünf explorativen 100%-Szenarien für die Forschungsvereinigung Verbrennungskraftmaschinen e.V. (FVV) Patrick R. Schmidt ∙ Werner Weindorf ∙ Werner Zittel LBST ∙ Ludwig-Bölkow-Systemtechnik GmbH ∙ Munich ∙ Germany 2016-11-23 ∙ WEB

Transcript

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

VDI-Fachtagung laquoInnovative Antrieberaquo ∙ Dresden ∙ 23 November 2016

Erneuerbare Energien im Verkehr 2050 Ergebnisse und Gedankenfutter aus fuumlnf explorativen 100-Szenarien fuumlr die Forschungsvereinigung Verbrennungskraftmaschinen eV (FVV)

Patrick R Schmidt ∙ Werner Weindorf ∙ Werner Zittel

BMVI ∙ German Federal Transport Ministry MKS ∙ German Mobility amp Fuels Strategy

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

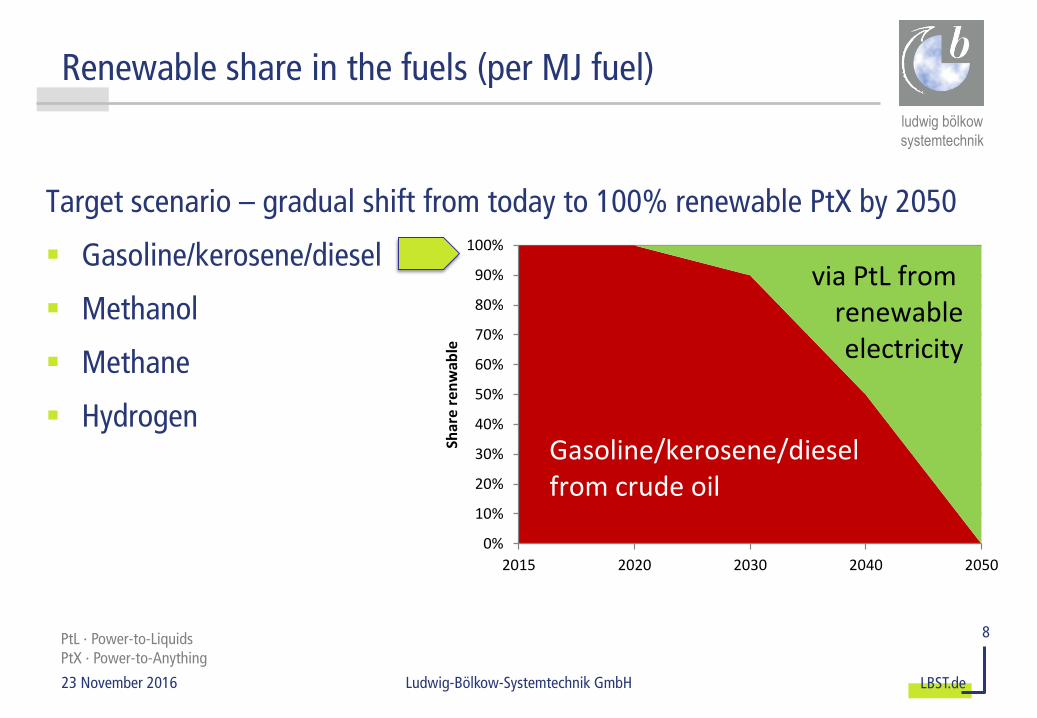

Target scenario ndash gradual shift from today to 100 renewable PtX by 2050

Gasolinekerosenediesel

Methanol

Methane

Hydrogen

0

10

20

30

40

50

60

70

80

90

100

2015 2020 2030 2040 2050

Shar

e r

en

wab

leGasolinekerosenedieselfrom crude oil

via PtL from renewableelectricity

Renewable share in the fuels (per MJ fuel)

8 PtL ∙ Power-to-Liquids PtX ∙ Power-to-Anything

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

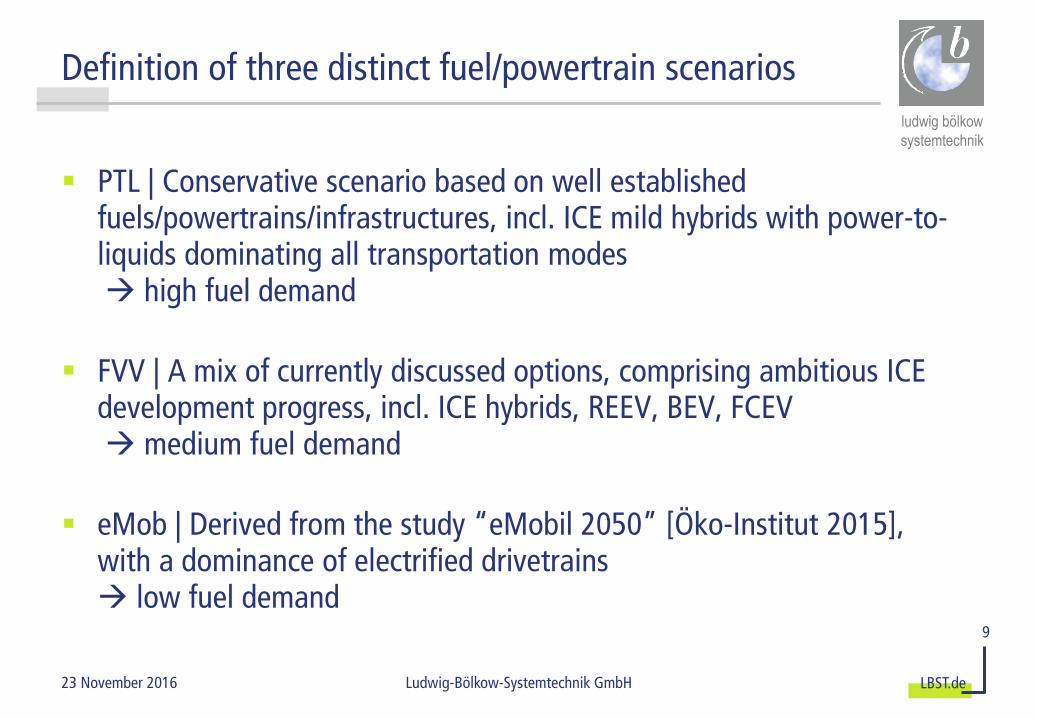

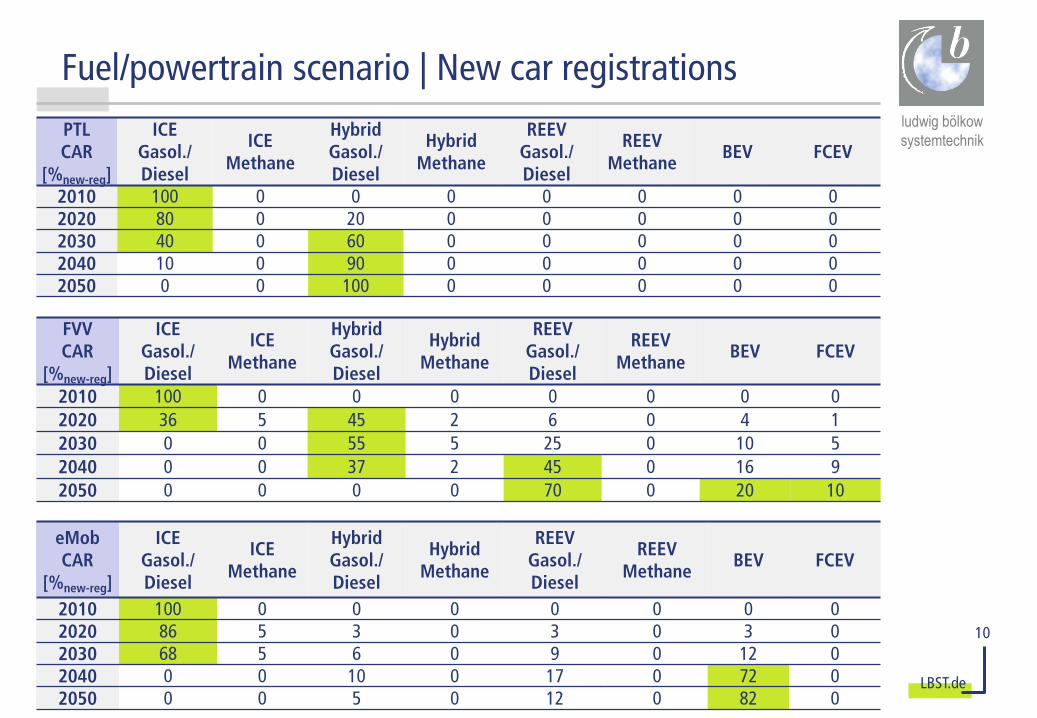

Definition of three distinct fuelpowertrain scenarios

PTL | Conservative scenario based on well established fuelspowertrainsinfrastructures incl ICE mild hybrids with power-to-liquids dominating all transportation modes high fuel demand

FVV | A mix of currently discussed options comprising ambitious ICE development progress incl ICE hybrids REEV BEV FCEV medium fuel demand

eMob | Derived from the study ldquoeMobil 2050rdquo [Oumlko-Institut 2015] with a dominance of electrified drivetrains low fuel demand

9

BEV ∙ Battery-electric vehicle eMob ∙ Electric mobility FCEV ∙ Fuel cell-electric vehicle FVV ∙ Research association PHEV ∙ Plug-in hybrid vehicle PTL ∙ Power-to-liquids REEV ∙ Range-extender vehicle

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

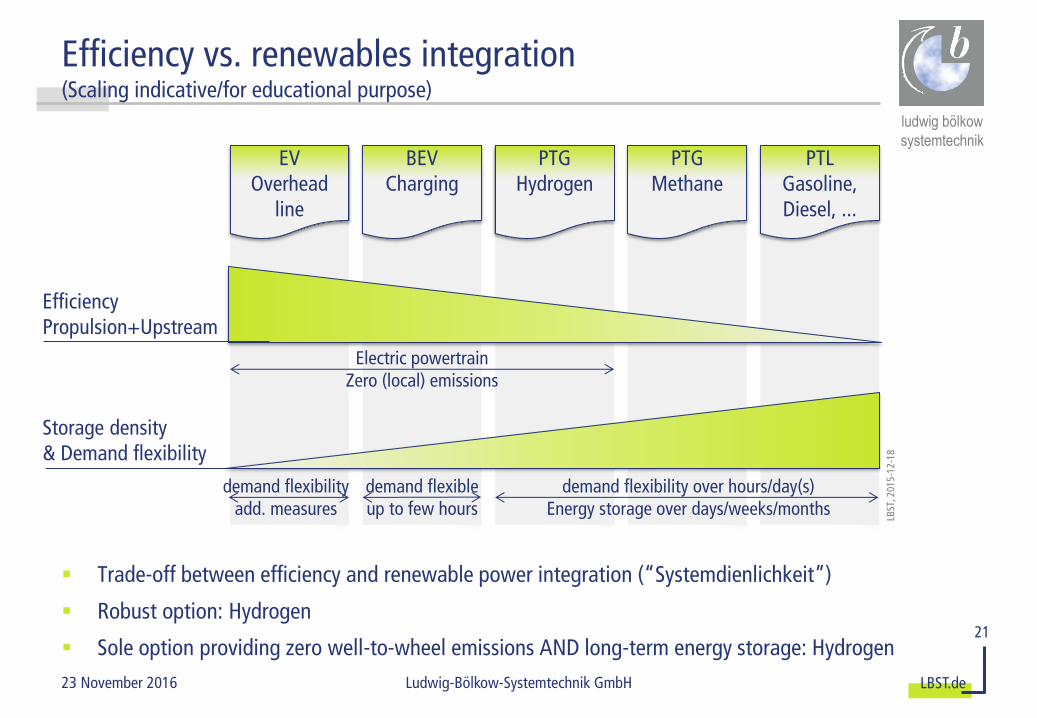

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

ANNEX

26

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Technical renewable power generation potentials

27

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany and EU-28

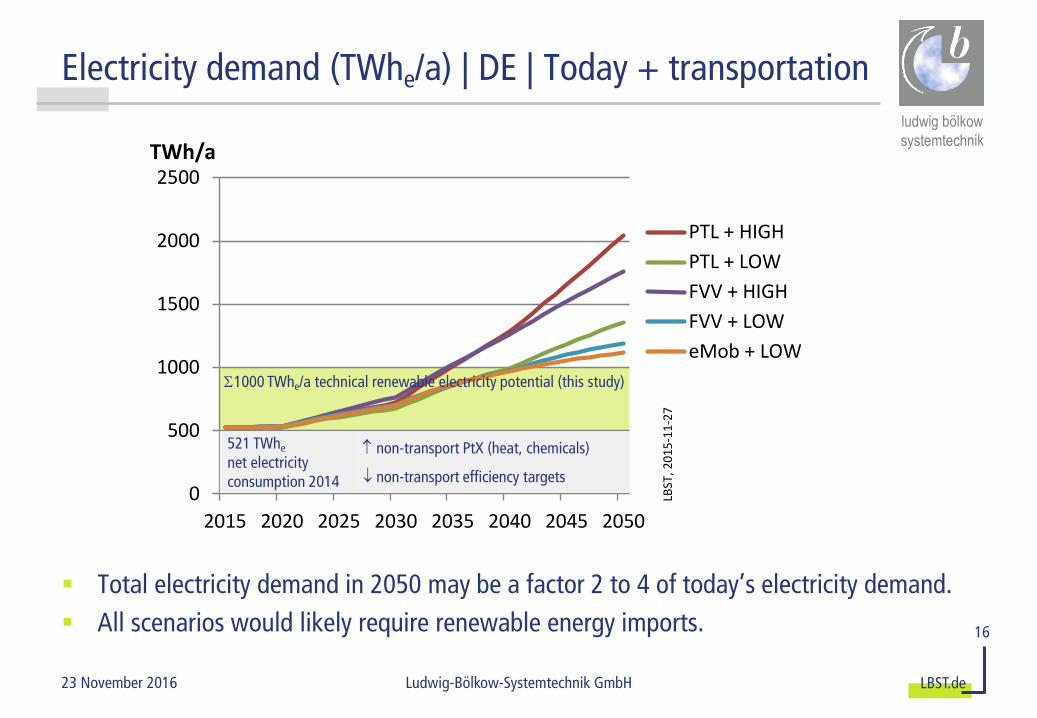

Germany and the EU have (very) high technical renewable electricity potentials

ndash DE ~1000 TWha potential vs ~500 TWh net electricity consumption

ndash EU ~11000 TWha potential vs ~2800 TWh net electricity consumption

Only ~11 (DE) and ~6 (EU28) if this potentials are currently used for renewable power production

The limits to renewable power growth seem to be more of an acceptance issue than costs

[ISE 2015] states PV electricity production costs of 2-4 euroctkWh in Southern and Central Europe by 2050

Renewable power potentials assessed for solarthermal power plants could also be exploited with photovoltaics

28

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

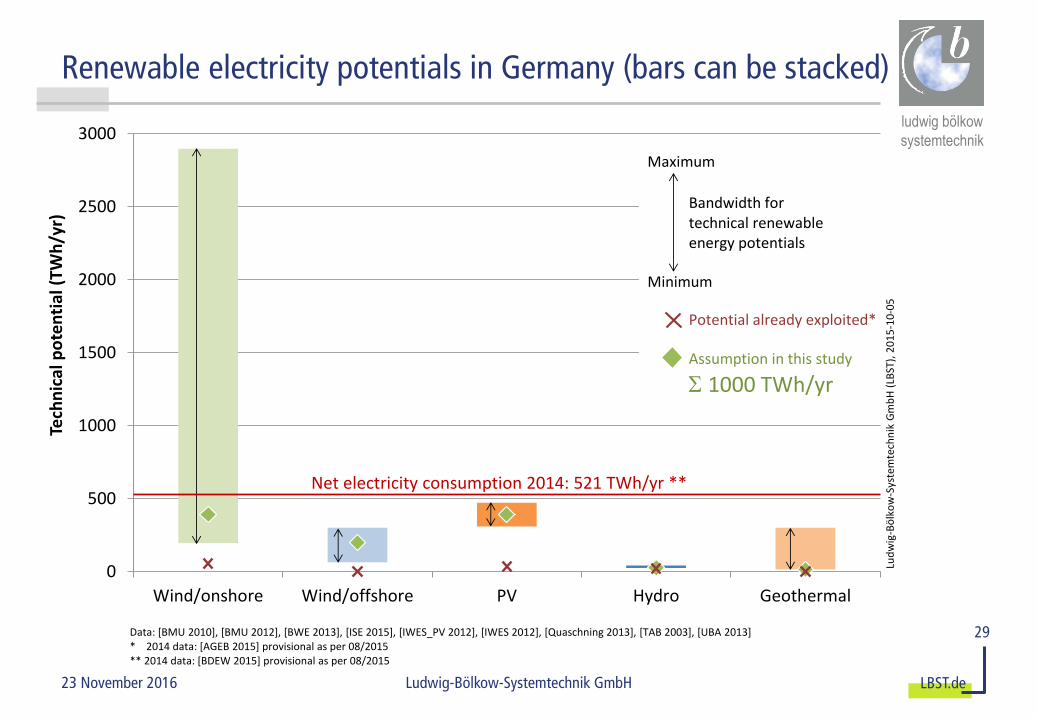

Renewable electricity potentials in Germany (bars can be stacked)

29

0

500

1000

1500

2000

2500

3000

Windonshore Windoffshore PV Hydro Geothermal

Tech

nic

al p

ote

nti

al (

TWh

yr)

Net electricity consumption 2014 521 TWhyr

Lud

wig

-Bouml

lko

w-S

yste

mte

chn

ik G

mb

H (

LBST

) 2

01

5-1

0-0

5

Maximum

Minimum

Bandwidth for technical renewableenergy potentials

Assumption in this study

1000 TWhyr

Potential already exploited

Data [BMU 2010] [BMU 2012] [BWE 2013] [ISE 2015] [IWES_PV 2012] [IWES 2012] [Quaschning 2013] [TAB 2003] [UBA 2013] 2014 data [AGEB 2015] provisional as per 082015 2014 data [BDEW 2015] provisional as per 082015

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

CO2 avoidance costs

30

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

BMVI ∙ German Federal Transport Ministry MKS ∙ German Mobility amp Fuels Strategy

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Target scenario ndash gradual shift from today to 100 renewable PtX by 2050

Gasolinekerosenediesel

Methanol

Methane

Hydrogen

0

10

20

30

40

50

60

70

80

90

100

2015 2020 2030 2040 2050

Shar

e r

en

wab

leGasolinekerosenedieselfrom crude oil

via PtL from renewableelectricity

Renewable share in the fuels (per MJ fuel)

8 PtL ∙ Power-to-Liquids PtX ∙ Power-to-Anything

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Definition of three distinct fuelpowertrain scenarios

PTL | Conservative scenario based on well established fuelspowertrainsinfrastructures incl ICE mild hybrids with power-to-liquids dominating all transportation modes high fuel demand

FVV | A mix of currently discussed options comprising ambitious ICE development progress incl ICE hybrids REEV BEV FCEV medium fuel demand

eMob | Derived from the study ldquoeMobil 2050rdquo [Oumlko-Institut 2015] with a dominance of electrified drivetrains low fuel demand

9

BEV ∙ Battery-electric vehicle eMob ∙ Electric mobility FCEV ∙ Fuel cell-electric vehicle FVV ∙ Research association PHEV ∙ Plug-in hybrid vehicle PTL ∙ Power-to-liquids REEV ∙ Range-extender vehicle

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

ANNEX

26

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Technical renewable power generation potentials

27

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany and EU-28

Germany and the EU have (very) high technical renewable electricity potentials

ndash DE ~1000 TWha potential vs ~500 TWh net electricity consumption

ndash EU ~11000 TWha potential vs ~2800 TWh net electricity consumption

Only ~11 (DE) and ~6 (EU28) if this potentials are currently used for renewable power production

The limits to renewable power growth seem to be more of an acceptance issue than costs

[ISE 2015] states PV electricity production costs of 2-4 euroctkWh in Southern and Central Europe by 2050

Renewable power potentials assessed for solarthermal power plants could also be exploited with photovoltaics

28

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany (bars can be stacked)

29

0

500

1000

1500

2000

2500

3000

Windonshore Windoffshore PV Hydro Geothermal

Tech

nic

al p

ote

nti

al (

TWh

yr)

Net electricity consumption 2014 521 TWhyr

Lud

wig

-Bouml

lko

w-S

yste

mte

chn

ik G

mb

H (

LBST

) 2

01

5-1

0-0

5

Maximum

Minimum

Bandwidth for technical renewableenergy potentials

Assumption in this study

1000 TWhyr

Potential already exploited

Data [BMU 2010] [BMU 2012] [BWE 2013] [ISE 2015] [IWES_PV 2012] [IWES 2012] [Quaschning 2013] [TAB 2003] [UBA 2013] 2014 data [AGEB 2015] provisional as per 082015 2014 data [BDEW 2015] provisional as per 082015

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

CO2 avoidance costs

30

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

BMVI ∙ German Federal Transport Ministry MKS ∙ German Mobility amp Fuels Strategy

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Target scenario ndash gradual shift from today to 100 renewable PtX by 2050

Gasolinekerosenediesel

Methanol

Methane

Hydrogen

0

10

20

30

40

50

60

70

80

90

100

2015 2020 2030 2040 2050

Shar

e r

en

wab

leGasolinekerosenedieselfrom crude oil

via PtL from renewableelectricity

Renewable share in the fuels (per MJ fuel)

8 PtL ∙ Power-to-Liquids PtX ∙ Power-to-Anything

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Definition of three distinct fuelpowertrain scenarios

PTL | Conservative scenario based on well established fuelspowertrainsinfrastructures incl ICE mild hybrids with power-to-liquids dominating all transportation modes high fuel demand

FVV | A mix of currently discussed options comprising ambitious ICE development progress incl ICE hybrids REEV BEV FCEV medium fuel demand

eMob | Derived from the study ldquoeMobil 2050rdquo [Oumlko-Institut 2015] with a dominance of electrified drivetrains low fuel demand

9

BEV ∙ Battery-electric vehicle eMob ∙ Electric mobility FCEV ∙ Fuel cell-electric vehicle FVV ∙ Research association PHEV ∙ Plug-in hybrid vehicle PTL ∙ Power-to-liquids REEV ∙ Range-extender vehicle

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

ANNEX

26

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Technical renewable power generation potentials

27

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany and EU-28

Germany and the EU have (very) high technical renewable electricity potentials

ndash DE ~1000 TWha potential vs ~500 TWh net electricity consumption

ndash EU ~11000 TWha potential vs ~2800 TWh net electricity consumption

Only ~11 (DE) and ~6 (EU28) if this potentials are currently used for renewable power production

The limits to renewable power growth seem to be more of an acceptance issue than costs

[ISE 2015] states PV electricity production costs of 2-4 euroctkWh in Southern and Central Europe by 2050

Renewable power potentials assessed for solarthermal power plants could also be exploited with photovoltaics

28

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany (bars can be stacked)

29

0

500

1000

1500

2000

2500

3000

Windonshore Windoffshore PV Hydro Geothermal

Tech

nic

al p

ote

nti

al (

TWh

yr)

Net electricity consumption 2014 521 TWhyr

Lud

wig

-Bouml

lko

w-S

yste

mte

chn

ik G

mb

H (

LBST

) 2

01

5-1

0-0

5

Maximum

Minimum

Bandwidth for technical renewableenergy potentials

Assumption in this study

1000 TWhyr

Potential already exploited

Data [BMU 2010] [BMU 2012] [BWE 2013] [ISE 2015] [IWES_PV 2012] [IWES 2012] [Quaschning 2013] [TAB 2003] [UBA 2013] 2014 data [AGEB 2015] provisional as per 082015 2014 data [BDEW 2015] provisional as per 082015

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

CO2 avoidance costs

30

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

BMVI ∙ German Federal Transport Ministry MKS ∙ German Mobility amp Fuels Strategy

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Target scenario ndash gradual shift from today to 100 renewable PtX by 2050

Gasolinekerosenediesel

Methanol

Methane

Hydrogen

0

10

20

30

40

50

60

70

80

90

100

2015 2020 2030 2040 2050

Shar

e r

en

wab

leGasolinekerosenedieselfrom crude oil

via PtL from renewableelectricity

Renewable share in the fuels (per MJ fuel)

8 PtL ∙ Power-to-Liquids PtX ∙ Power-to-Anything

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Definition of three distinct fuelpowertrain scenarios

PTL | Conservative scenario based on well established fuelspowertrainsinfrastructures incl ICE mild hybrids with power-to-liquids dominating all transportation modes high fuel demand

FVV | A mix of currently discussed options comprising ambitious ICE development progress incl ICE hybrids REEV BEV FCEV medium fuel demand

eMob | Derived from the study ldquoeMobil 2050rdquo [Oumlko-Institut 2015] with a dominance of electrified drivetrains low fuel demand

9

BEV ∙ Battery-electric vehicle eMob ∙ Electric mobility FCEV ∙ Fuel cell-electric vehicle FVV ∙ Research association PHEV ∙ Plug-in hybrid vehicle PTL ∙ Power-to-liquids REEV ∙ Range-extender vehicle

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

ANNEX

26

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Technical renewable power generation potentials

27

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany and EU-28

Germany and the EU have (very) high technical renewable electricity potentials

ndash DE ~1000 TWha potential vs ~500 TWh net electricity consumption

ndash EU ~11000 TWha potential vs ~2800 TWh net electricity consumption

Only ~11 (DE) and ~6 (EU28) if this potentials are currently used for renewable power production

The limits to renewable power growth seem to be more of an acceptance issue than costs

[ISE 2015] states PV electricity production costs of 2-4 euroctkWh in Southern and Central Europe by 2050

Renewable power potentials assessed for solarthermal power plants could also be exploited with photovoltaics

28

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany (bars can be stacked)

29

0

500

1000

1500

2000

2500

3000

Windonshore Windoffshore PV Hydro Geothermal

Tech

nic

al p

ote

nti

al (

TWh

yr)

Net electricity consumption 2014 521 TWhyr

Lud

wig

-Bouml

lko

w-S

yste

mte

chn

ik G

mb

H (

LBST

) 2

01

5-1

0-0

5

Maximum

Minimum

Bandwidth for technical renewableenergy potentials

Assumption in this study

1000 TWhyr

Potential already exploited

Data [BMU 2010] [BMU 2012] [BWE 2013] [ISE 2015] [IWES_PV 2012] [IWES 2012] [Quaschning 2013] [TAB 2003] [UBA 2013] 2014 data [AGEB 2015] provisional as per 082015 2014 data [BDEW 2015] provisional as per 082015

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

CO2 avoidance costs

30

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

BMVI ∙ German Federal Transport Ministry MKS ∙ German Mobility amp Fuels Strategy

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Target scenario ndash gradual shift from today to 100 renewable PtX by 2050

Gasolinekerosenediesel

Methanol

Methane

Hydrogen

0

10

20

30

40

50

60

70

80

90

100

2015 2020 2030 2040 2050

Shar

e r

en

wab

leGasolinekerosenedieselfrom crude oil

via PtL from renewableelectricity

Renewable share in the fuels (per MJ fuel)

8 PtL ∙ Power-to-Liquids PtX ∙ Power-to-Anything

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Definition of three distinct fuelpowertrain scenarios

PTL | Conservative scenario based on well established fuelspowertrainsinfrastructures incl ICE mild hybrids with power-to-liquids dominating all transportation modes high fuel demand

FVV | A mix of currently discussed options comprising ambitious ICE development progress incl ICE hybrids REEV BEV FCEV medium fuel demand

eMob | Derived from the study ldquoeMobil 2050rdquo [Oumlko-Institut 2015] with a dominance of electrified drivetrains low fuel demand

9

BEV ∙ Battery-electric vehicle eMob ∙ Electric mobility FCEV ∙ Fuel cell-electric vehicle FVV ∙ Research association PHEV ∙ Plug-in hybrid vehicle PTL ∙ Power-to-liquids REEV ∙ Range-extender vehicle

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

ANNEX

26

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Technical renewable power generation potentials

27

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany and EU-28

Germany and the EU have (very) high technical renewable electricity potentials

ndash DE ~1000 TWha potential vs ~500 TWh net electricity consumption

ndash EU ~11000 TWha potential vs ~2800 TWh net electricity consumption

Only ~11 (DE) and ~6 (EU28) if this potentials are currently used for renewable power production

The limits to renewable power growth seem to be more of an acceptance issue than costs

[ISE 2015] states PV electricity production costs of 2-4 euroctkWh in Southern and Central Europe by 2050

Renewable power potentials assessed for solarthermal power plants could also be exploited with photovoltaics

28

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany (bars can be stacked)

29

0

500

1000

1500

2000

2500

3000

Windonshore Windoffshore PV Hydro Geothermal

Tech

nic

al p

ote

nti

al (

TWh

yr)

Net electricity consumption 2014 521 TWhyr

Lud

wig

-Bouml

lko

w-S

yste

mte

chn

ik G

mb

H (

LBST

) 2

01

5-1

0-0

5

Maximum

Minimum

Bandwidth for technical renewableenergy potentials

Assumption in this study

1000 TWhyr

Potential already exploited

Data [BMU 2010] [BMU 2012] [BWE 2013] [ISE 2015] [IWES_PV 2012] [IWES 2012] [Quaschning 2013] [TAB 2003] [UBA 2013] 2014 data [AGEB 2015] provisional as per 082015 2014 data [BDEW 2015] provisional as per 082015

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

CO2 avoidance costs

30

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

BMVI ∙ German Federal Transport Ministry MKS ∙ German Mobility amp Fuels Strategy

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Target scenario ndash gradual shift from today to 100 renewable PtX by 2050

Gasolinekerosenediesel

Methanol

Methane

Hydrogen

0

10

20

30

40

50

60

70

80

90

100

2015 2020 2030 2040 2050

Shar

e r

en

wab

leGasolinekerosenedieselfrom crude oil

via PtL from renewableelectricity

Renewable share in the fuels (per MJ fuel)

8 PtL ∙ Power-to-Liquids PtX ∙ Power-to-Anything

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Definition of three distinct fuelpowertrain scenarios

PTL | Conservative scenario based on well established fuelspowertrainsinfrastructures incl ICE mild hybrids with power-to-liquids dominating all transportation modes high fuel demand

FVV | A mix of currently discussed options comprising ambitious ICE development progress incl ICE hybrids REEV BEV FCEV medium fuel demand

eMob | Derived from the study ldquoeMobil 2050rdquo [Oumlko-Institut 2015] with a dominance of electrified drivetrains low fuel demand

9

BEV ∙ Battery-electric vehicle eMob ∙ Electric mobility FCEV ∙ Fuel cell-electric vehicle FVV ∙ Research association PHEV ∙ Plug-in hybrid vehicle PTL ∙ Power-to-liquids REEV ∙ Range-extender vehicle

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

ANNEX

26

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Technical renewable power generation potentials

27

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany and EU-28

Germany and the EU have (very) high technical renewable electricity potentials

ndash DE ~1000 TWha potential vs ~500 TWh net electricity consumption

ndash EU ~11000 TWha potential vs ~2800 TWh net electricity consumption

Only ~11 (DE) and ~6 (EU28) if this potentials are currently used for renewable power production

The limits to renewable power growth seem to be more of an acceptance issue than costs

[ISE 2015] states PV electricity production costs of 2-4 euroctkWh in Southern and Central Europe by 2050

Renewable power potentials assessed for solarthermal power plants could also be exploited with photovoltaics

28

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany (bars can be stacked)

29

0

500

1000

1500

2000

2500

3000

Windonshore Windoffshore PV Hydro Geothermal

Tech

nic

al p

ote

nti

al (

TWh

yr)

Net electricity consumption 2014 521 TWhyr

Lud

wig

-Bouml

lko

w-S

yste

mte

chn

ik G

mb

H (

LBST

) 2

01

5-1

0-0

5

Maximum

Minimum

Bandwidth for technical renewableenergy potentials

Assumption in this study

1000 TWhyr

Potential already exploited

Data [BMU 2010] [BMU 2012] [BWE 2013] [ISE 2015] [IWES_PV 2012] [IWES 2012] [Quaschning 2013] [TAB 2003] [UBA 2013] 2014 data [AGEB 2015] provisional as per 082015 2014 data [BDEW 2015] provisional as per 082015

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

CO2 avoidance costs

30

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

BMVI ∙ German Federal Transport Ministry MKS ∙ German Mobility amp Fuels Strategy

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Target scenario ndash gradual shift from today to 100 renewable PtX by 2050

Gasolinekerosenediesel

Methanol

Methane

Hydrogen

0

10

20

30

40

50

60

70

80

90

100

2015 2020 2030 2040 2050

Shar

e r

en

wab

leGasolinekerosenedieselfrom crude oil

via PtL from renewableelectricity

Renewable share in the fuels (per MJ fuel)

8 PtL ∙ Power-to-Liquids PtX ∙ Power-to-Anything

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Definition of three distinct fuelpowertrain scenarios

PTL | Conservative scenario based on well established fuelspowertrainsinfrastructures incl ICE mild hybrids with power-to-liquids dominating all transportation modes high fuel demand

FVV | A mix of currently discussed options comprising ambitious ICE development progress incl ICE hybrids REEV BEV FCEV medium fuel demand

eMob | Derived from the study ldquoeMobil 2050rdquo [Oumlko-Institut 2015] with a dominance of electrified drivetrains low fuel demand

9

BEV ∙ Battery-electric vehicle eMob ∙ Electric mobility FCEV ∙ Fuel cell-electric vehicle FVV ∙ Research association PHEV ∙ Plug-in hybrid vehicle PTL ∙ Power-to-liquids REEV ∙ Range-extender vehicle

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

ANNEX

26

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Technical renewable power generation potentials

27

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany and EU-28

Germany and the EU have (very) high technical renewable electricity potentials

ndash DE ~1000 TWha potential vs ~500 TWh net electricity consumption

ndash EU ~11000 TWha potential vs ~2800 TWh net electricity consumption

Only ~11 (DE) and ~6 (EU28) if this potentials are currently used for renewable power production

The limits to renewable power growth seem to be more of an acceptance issue than costs

[ISE 2015] states PV electricity production costs of 2-4 euroctkWh in Southern and Central Europe by 2050

Renewable power potentials assessed for solarthermal power plants could also be exploited with photovoltaics

28

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany (bars can be stacked)

29

0

500

1000

1500

2000

2500

3000

Windonshore Windoffshore PV Hydro Geothermal

Tech

nic

al p

ote

nti

al (

TWh

yr)

Net electricity consumption 2014 521 TWhyr

Lud

wig

-Bouml

lko

w-S

yste

mte

chn

ik G

mb

H (

LBST

) 2

01

5-1

0-0

5

Maximum

Minimum

Bandwidth for technical renewableenergy potentials

Assumption in this study

1000 TWhyr

Potential already exploited

Data [BMU 2010] [BMU 2012] [BWE 2013] [ISE 2015] [IWES_PV 2012] [IWES 2012] [Quaschning 2013] [TAB 2003] [UBA 2013] 2014 data [AGEB 2015] provisional as per 082015 2014 data [BDEW 2015] provisional as per 082015

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

CO2 avoidance costs

30

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

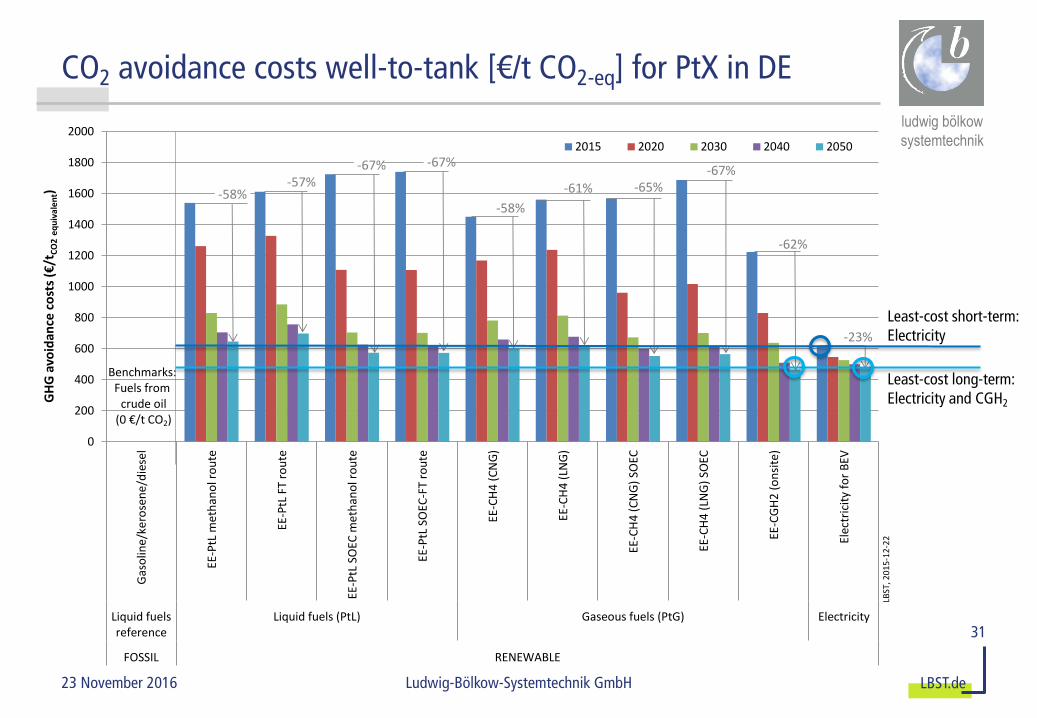

CO2 avoidance costs well-to-tank [eurot CO2-eq] for PtX in DE

31

Least-cost short-term Electricity

Least-cost long-term Electricity and CGH2

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Target scenario ndash gradual shift from today to 100 renewable PtX by 2050

Gasolinekerosenediesel

Methanol

Methane

Hydrogen

0

10

20

30

40

50

60

70

80

90

100

2015 2020 2030 2040 2050

Shar

e r

en

wab

leGasolinekerosenedieselfrom crude oil

via PtL from renewableelectricity

Renewable share in the fuels (per MJ fuel)

8 PtL ∙ Power-to-Liquids PtX ∙ Power-to-Anything

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Definition of three distinct fuelpowertrain scenarios

PTL | Conservative scenario based on well established fuelspowertrainsinfrastructures incl ICE mild hybrids with power-to-liquids dominating all transportation modes high fuel demand

FVV | A mix of currently discussed options comprising ambitious ICE development progress incl ICE hybrids REEV BEV FCEV medium fuel demand

eMob | Derived from the study ldquoeMobil 2050rdquo [Oumlko-Institut 2015] with a dominance of electrified drivetrains low fuel demand

9

BEV ∙ Battery-electric vehicle eMob ∙ Electric mobility FCEV ∙ Fuel cell-electric vehicle FVV ∙ Research association PHEV ∙ Plug-in hybrid vehicle PTL ∙ Power-to-liquids REEV ∙ Range-extender vehicle

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

ANNEX

26

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Technical renewable power generation potentials

27

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany and EU-28

Germany and the EU have (very) high technical renewable electricity potentials

ndash DE ~1000 TWha potential vs ~500 TWh net electricity consumption

ndash EU ~11000 TWha potential vs ~2800 TWh net electricity consumption

Only ~11 (DE) and ~6 (EU28) if this potentials are currently used for renewable power production

The limits to renewable power growth seem to be more of an acceptance issue than costs

[ISE 2015] states PV electricity production costs of 2-4 euroctkWh in Southern and Central Europe by 2050

Renewable power potentials assessed for solarthermal power plants could also be exploited with photovoltaics

28

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany (bars can be stacked)

29

0

500

1000

1500

2000

2500

3000

Windonshore Windoffshore PV Hydro Geothermal

Tech

nic

al p

ote

nti

al (

TWh

yr)

Net electricity consumption 2014 521 TWhyr

Lud

wig

-Bouml

lko

w-S

yste

mte

chn

ik G

mb

H (

LBST

) 2

01

5-1

0-0

5

Maximum

Minimum

Bandwidth for technical renewableenergy potentials

Assumption in this study

1000 TWhyr

Potential already exploited

Data [BMU 2010] [BMU 2012] [BWE 2013] [ISE 2015] [IWES_PV 2012] [IWES 2012] [Quaschning 2013] [TAB 2003] [UBA 2013] 2014 data [AGEB 2015] provisional as per 082015 2014 data [BDEW 2015] provisional as per 082015

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

CO2 avoidance costs

30

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

CO2 avoidance costs well-to-tank [eurot CO2-eq] for PtX in DE

31

Least-cost short-term Electricity

Least-cost long-term Electricity and CGH2

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Definition of three distinct fuelpowertrain scenarios

PTL | Conservative scenario based on well established fuelspowertrainsinfrastructures incl ICE mild hybrids with power-to-liquids dominating all transportation modes high fuel demand

FVV | A mix of currently discussed options comprising ambitious ICE development progress incl ICE hybrids REEV BEV FCEV medium fuel demand

eMob | Derived from the study ldquoeMobil 2050rdquo [Oumlko-Institut 2015] with a dominance of electrified drivetrains low fuel demand

9

BEV ∙ Battery-electric vehicle eMob ∙ Electric mobility FCEV ∙ Fuel cell-electric vehicle FVV ∙ Research association PHEV ∙ Plug-in hybrid vehicle PTL ∙ Power-to-liquids REEV ∙ Range-extender vehicle

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

ANNEX

26

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Technical renewable power generation potentials

27

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany and EU-28

Germany and the EU have (very) high technical renewable electricity potentials

ndash DE ~1000 TWha potential vs ~500 TWh net electricity consumption

ndash EU ~11000 TWha potential vs ~2800 TWh net electricity consumption

Only ~11 (DE) and ~6 (EU28) if this potentials are currently used for renewable power production

The limits to renewable power growth seem to be more of an acceptance issue than costs

[ISE 2015] states PV electricity production costs of 2-4 euroctkWh in Southern and Central Europe by 2050

Renewable power potentials assessed for solarthermal power plants could also be exploited with photovoltaics

28

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany (bars can be stacked)

29

0

500

1000

1500

2000

2500

3000

Windonshore Windoffshore PV Hydro Geothermal

Tech

nic

al p

ote

nti

al (

TWh

yr)

Net electricity consumption 2014 521 TWhyr

Lud

wig

-Bouml

lko

w-S

yste

mte

chn

ik G

mb

H (

LBST

) 2

01

5-1

0-0

5

Maximum

Minimum

Bandwidth for technical renewableenergy potentials

Assumption in this study

1000 TWhyr

Potential already exploited

Data [BMU 2010] [BMU 2012] [BWE 2013] [ISE 2015] [IWES_PV 2012] [IWES 2012] [Quaschning 2013] [TAB 2003] [UBA 2013] 2014 data [AGEB 2015] provisional as per 082015 2014 data [BDEW 2015] provisional as per 082015

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

CO2 avoidance costs

30

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

ANNEX

26

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Technical renewable power generation potentials

27

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany and EU-28

Germany and the EU have (very) high technical renewable electricity potentials

ndash DE ~1000 TWha potential vs ~500 TWh net electricity consumption

ndash EU ~11000 TWha potential vs ~2800 TWh net electricity consumption

Only ~11 (DE) and ~6 (EU28) if this potentials are currently used for renewable power production

The limits to renewable power growth seem to be more of an acceptance issue than costs

[ISE 2015] states PV electricity production costs of 2-4 euroctkWh in Southern and Central Europe by 2050

Renewable power potentials assessed for solarthermal power plants could also be exploited with photovoltaics

28

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany (bars can be stacked)

29

0

500

1000

1500

2000

2500

3000

Windonshore Windoffshore PV Hydro Geothermal

Tech

nic

al p

ote

nti

al (

TWh

yr)

Net electricity consumption 2014 521 TWhyr

Lud

wig

-Bouml

lko

w-S

yste

mte

chn

ik G

mb

H (

LBST

) 2

01

5-1

0-0

5

Maximum

Minimum

Bandwidth for technical renewableenergy potentials

Assumption in this study

1000 TWhyr

Potential already exploited

Data [BMU 2010] [BMU 2012] [BWE 2013] [ISE 2015] [IWES_PV 2012] [IWES 2012] [Quaschning 2013] [TAB 2003] [UBA 2013] 2014 data [AGEB 2015] provisional as per 082015 2014 data [BDEW 2015] provisional as per 082015

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

CO2 avoidance costs

30

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

ANNEX

26

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Technical renewable power generation potentials

27

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany and EU-28

Germany and the EU have (very) high technical renewable electricity potentials

ndash DE ~1000 TWha potential vs ~500 TWh net electricity consumption

ndash EU ~11000 TWha potential vs ~2800 TWh net electricity consumption

Only ~11 (DE) and ~6 (EU28) if this potentials are currently used for renewable power production

The limits to renewable power growth seem to be more of an acceptance issue than costs

[ISE 2015] states PV electricity production costs of 2-4 euroctkWh in Southern and Central Europe by 2050

Renewable power potentials assessed for solarthermal power plants could also be exploited with photovoltaics

28

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Renewable electricity potentials in Germany (bars can be stacked)

29

0

500

1000

1500

2000

2500

3000

Windonshore Windoffshore PV Hydro Geothermal

Tech

nic

al p

ote

nti

al (

TWh

yr)

Net electricity consumption 2014 521 TWhyr

Lud

wig

-Bouml

lko

w-S

yste

mte

chn

ik G

mb

H (

LBST

) 2

01

5-1

0-0

5

Maximum

Minimum

Bandwidth for technical renewableenergy potentials

Assumption in this study

1000 TWhyr

Potential already exploited

Data [BMU 2010] [BMU 2012] [BWE 2013] [ISE 2015] [IWES_PV 2012] [IWES 2012] [Quaschning 2013] [TAB 2003] [UBA 2013] 2014 data [AGEB 2015] provisional as per 082015 2014 data [BDEW 2015] provisional as per 082015

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

CO2 avoidance costs

30

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

System integration of fluctating renewable power generation

20

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Efficiency vs renewables integration (Scaling indicativefor educational purpose)

Trade-off between efficiency and renewable power integration (ldquoSystemdienlichkeitrdquo)

Robust option Hydrogen

Sole option providing zero well-to-wheel emissions AND long-term energy storage Hydrogen

BEV battery-electric vehicle EV electric vehicle DSM demand-side management PTG power-to-gas PTL power-to-liquids

Electric powertrain Zero (local) emissions

demand flexible up to few hours

demand flexibility over hoursday(s) Energy storage over daysweeksmonths

demand flexibility add measures

LBST

201

5-12

-18

EV Overhead

line

BEV Charging

PTG Hydrogen

PTG Methane

PTL Gasoline Diesel

Efficiency Propulsion+Upstream

Storage density amp Demand flexibility

21

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Agenda

1 Motivation and approach

2 Scenarios

3 Results

Greenhouse gas emissions

Energy demand

Cumulated investments

4 Conclusions

22

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Conclusions from the FVV Future Fuel study in a nutshell

Transportation demand development (pkm tkm) is strongest driver for fuelelectricity demand

PtX fuel costs could half between 2015 and 2050 PtL imports ~20 lower in cost Further cost reductions are subject to location-specific business cases

PtX costs are dominated by electricity costs which strongly depends on the fuel choice (H2 CH4 PTL) and associated plant efficiencies

Fuel distribution infrastructure costs are negligible compared to the upstream investments required for any of the scenarios analysed

Cumulated investments for Energiewende (energy transition) in the transportation sector seem manageable for any of the scenarios analysed

All scenarios analysed will probably exceed technicalacceptable renewable electricity potentials in Germany Import of PtL (if any) is likely for cost reasons

Transport must get more electric with regard to the fuel and the propulsion system

23 pkm ∙ person kilometre tkm ∙ tonne kilometre PtX ∙ Power-to-anything PtL ∙ Power-to-liquids

LBSTde 23 November 2016 Ludwig-Boumllkow-Systemtechnik GmbH

ludwig boumllkow

systemtechnik

Literature

P Schmidt W Zittel W Weindorf T Raksha (LBST)

Renewables in Transport 2050 ndash Empowering a sustainable mobility future with zero emission fuels from renewable electricity ndash Europe and Germany

Research Association for Combustion Engines eV (ed)

This study was financed by the FVV and supported by members of the FVV Working Group laquoFuture Fuelsraquo